9 Reasons Why Stay-at-Home Parents Need Life Insurance

It's not just parents with full-time jobs that need life insurance. Stay-at-home parents also need coverage. Read this blog post for 9 reasons why stay-at-home parents should have life insurance as well.

You’re probably already aware that a parent with a job outside the house most likely needs life insurance to protect their loved ones in case something were to happen. But it’s not just breadwinners who need coverage—stay-at-home parents do, too. Here are nine reasons why.

1. To replace the value of their labor. Stay-at-home parents are caretakers, tutors, cooks, housekeepers, chauffeurs, and so much more 365 days a year. And all that work comes with a price tag: Salary.com reports that stay-at-home-parents contribute the equivalent of a $162,581 annual salary to their households. If the unthinkable were to happen, a surviving partner would be on the hook for a slew of new expenses that the stay-at-home parent previously shouldered. Term life insurance is generally a quick and affordable way to get a substantial amount of coverage like this for a specific period of time, such as 10 or 20 years—often until you pay of your mortgage or the kids are grown and gone.

2. To factor in the contributions of any future income. Many stay-at-home parents return to the workforce once their kids are older. Life insurance could help bridge the gap that their future earnings would have contributed to the household.

3. To pay off any debt. From student loans to credit card debt to an informal loan from a family member, there are lots of ways to owe money. Life insurance can help settle any debts left behind so they don’t create stress for grieving loved ones.

4. To cover funeral expenses. Would you believe that the average funeral runs between $7,000 and $10,000, according to parting.com? And that may not cover the cost of the burial, headstone and other expenses. Many families want to honor a loved one’s memory but have trouble finding the funds to cover all the costs. Fortunately, the payout from a life insurance policy can help cover final wishes.

5. To leave a legacy. If a stay-at-home spouse has a passion for a place of worship, an alma mater, or another nonprofit organization, life insurance proceeds can be used to leave a meaningful charitable gift.

6. To boost savings. Permanent life insurance, which offers lifelong protection as long as you pay your premiums, may offer additional living benefits such as the ability to build cash value. This can be used in the future for any purpose you wish, from making a down payment on a house to paying for college tuition. Keep in mind, though, that withdrawing or borrowing funds will reduce your policy’s cash value and death benefit if not repaid.

7. To guarantee insurability. Your health can change in an instant. Getting a permanent life insurance policy when you’re young and healthy means you’ll have lifelong coverage. Then you won’t have to worry if later on, you develop a health condition that would make it hard or even impossible to get life insurance.

8. To receive tax-free benefits. Life insurance is one of the few ways to leave loved one's money that is generally income-tax free.

9. To give loved ones peace of mind. Losing a parent and partner before their time is already hard enough without having to worry about unsettled debts, childcare costs, funeral bills, and other expenses.

As you can see, life insurance for stay-at-home parents is just as important as it is for parents who work outside the home. Schedule a time to talk with an insurance professional in your community to learn about your options and get coverage that fits your lifestyle and budget.

SOURCE: Austin, A. (11 December 2018) "9 Reasons Why Stay-at-Home Parents Need Life Insurance" (Web Blog Post). Retrieved from https://lifehappens.org/blog/9-reasons-why-stay-at-home-parents-need-life-insurance-2/

Denied Life Insurance? Here Are Your Next 3 Steps

Were you denied life insurance coverage? Many applicants who fall into the “impaired risk market” understand they're up against a hurdle or two when applying for life insurance, but it doesn't make it any easier when they're denied coverage. Read this blog post for the next steps you should take after being denied life insurance coverage.

It’s tough to learn that the life insurance company you applied to will not be offering you coverage, especially if you were fully expecting a yes!

You may fall into the “impaired risk market,” which means you have something in your background that makes you a higher risk for dying prematurely—think things like diabetes, obesity, a previous cancer diagnosis or even a history of DUIs.

While many applicants with this type of history understand they’re up against a hurdle or two, it’s not any easier to be denied life insurance coverage. But, often times, it doesn’t mean the hunt for an approval is over.

There may still be options, which include applying to a more suitable company or applying for a different policy type.

Here are three actionable steps you should take if you’ve been denied life insurance.

1. Collect information. Before an insurer denies an application, they collect lots of data from several sources to evaluate your risk. If the risk is high enough, you are either rated, postponed or denied. In any of these circumstances, requesting more information on the reason for denial is your right.

Upon request, the carrier can provide detailed information on why an applicant is declined, whether it was due to medical history, current exam results, driving record or something else. Denials from current exams tend to be the most shocking, as you may not know about an illness or disease beforehand.

2. Confirm the results. Errors can happen. Wires can be crossed. Double check the data that was provided to the underwriter. If poor exam results were cited as the cause, confirm it with your primary care physician. In some cases, a company may simply deny coverage because of new, undiagnosed lab results, even if there is little cause for concern.

In other scenarios, you could be denied for occupational or recreational hazards, criminal records and even financial distress. Having records such as these, which aren’t updated or detailed enough, can lead to postponement or declines because the underwriter simply can’t assess a proper risk profile.

3. Work with an agent. Even with proper research, the first company you apply to isn’t always necessarily the best. Passing along detailed information to an agent can allow them to search into better options. A well-trained high-risk life insurance agent can assess information thoroughly and find a better fit for you.

But you also need to understand that applying to another carrier is an option only if the reason for denial (such a diabetes) is one another may accept (because your diabetes is under control with medication). Each life insurance company adheres to its own set of underwriting guidelines, meaning identical applications to separate carriers could yield different results.

If the root cause for denial is too great, a different type of life insurance policy altogether may be the last resort. Utilizing “graded” or guaranteed products make life insurance possible for those with pre-existing conditions or unfavorable risk profiles. While they cost more and typically come with maximum death benefits, they can be a solution.

Saving in the Long Run

After being approved for life insurance, keep an eye out over the next few months or years. Depending on your situation, you might have options to lower your rate. Here two quick examples:

Let time pass. Certain impaired risks simply require more time to pass between diagnosis and the time of application. As medical records and follow-ups are recorded, and symptoms pass or become stable, your rates can come back down. In addition, concerns related to a driving record or criminal record may also just require a certain amount to have elapsed where the offense is either removed or settled.

Check the workplace. If life insurance is offered through group benefits in the workplace, it could end up being more affordable, based on the program offered. It could also lead to filling in coverage gaps a graded or guaranteed policy left behind.

There is no one-size-fits-all regimen to combat a declination. However, taking these steps could alleviate the stress and annoyances that make finding coverage so daunting.

SOURCE: Fisher, J. (10 June 2019) "Denied Life Insurance? Here Are Your Next 3 Steps" (Web Blog Post). Retrieved from https://lifehappens.org/blog/denied-life-insurance-here-are-your-next-3-steps/

Seeing beyond size in vision care networks

How do you measure the quality of your vision care network? When it comes to the world of vision care, size isn't the only factor to consider when deciding which network best fits the needs of your employees. Read on to learn more.

Most people believe that “size matters” in regards to provider networks, but in the world of vision care, there are other important factors to consider when deciding which network matches the needs of employees. Network members usually see their vision provider for routine services just once per year. When an employer changes vision administrators, employee in-network utilization is more than 90% regardless of the new network size. Why? Employees are not concerned about changing providers to access in-network benefits. Plus, the new vision provider network will always provide access to multiple providers wherever the employee lives and works.

But what about the quality of the vision care network? To properly assess this measurement of competing networks, employers and benefits advisors need to ask several different questions.

Determine the network’s quality

The quality of the network is vital. Start asking these questions: How are vision care providers credentialed? Do they follow the National Committee for Quality Assurance (NCQA) guidelines developed to improve healthcare quality? Are there provider audit programs provided on an ongoing basis? Is the vision care provider re-credentialed and how often? How frequently are reviews conducted of the Office of Inspector General and Medicare and Medicaid disbarment lists?

Establish the network’s effectiveness

Once you know you have a quality network, now you must ask how effective the network is. How diverse is the network? Are there ample ophthalmologists, optometrists and optical retailers we can access? Are some private practitioners? You want to make sure that a solid provider mix is available to give employees options when choosing a vision care provider.

It’s critical to know what languages are spoken within the employee population as well as the providers who care for them. If you have a large population who speak a certain language you want to make sure your network gives them access to people who can truly understand them and with whom they feel comfortable.

Finally, look at the hours of operations. With schedules being busier now than ever before, people need flexibility when it comes to visiting hours. Do they offer evening hours? Weekend hours? This is particularly important for single parents who work during the week and need the flexibility to visit an eye care professional with his or her child after work.

Having a diverse, quality vision care provider network with convenient access helps keep employees happy, healthy and in-network.

Other factors to consider

One of the other factors to be cognizant of is network ownership. Today, many managed vision care companies are involved in not only providing coverage for vision care but also in delivering it. This means the vision benefits company you’re considering may own optical laboratories, frame companies or retail locations, which can pose conflicts of interest between you, your employees and the managed vision care company. Their need to produce profits can lead to undo pressure on your employees to purchase expensive and potentially unnecessary lens types, materials and options. Coupled with direct to consumer advertising and the expansion of brands, eyeglasses have become even more expensive.

This leads to another factor for consideration. Does the potential vision benefit administrator provide meaningful information to help your employees make informed decisions about what they really need, when it comes to the myriad of options available for frames, lenses and lens options?

Network matching

Start by remembering two things when matching networks. First, if you’ve changed vision carriers in the past, you selected a network that was not identical to your previous one. Vision networks never match each other. Some have higher proportions of independent providers and lower percentages of large retailer chains. Second, the infrequency with which the vision benefit is available to be used mitigates the impact of changing providers. People don’t have the same attachment to their eye care professional as they do with their physician.

Beyond quality and effectiveness is the important factor of access. The vision industry has grown to a point where there are often many more providers than would ever be necessary to provide convenient access for your membership. The reality is that two networks may be equally sized in an area and yet there may be little overlap, making the selection of the best network with the lowest overall cost a better strategic direction than simply selecting the one with the highest provider match.

The vision industry has long demonstrated that employees are willing to select new providers, especially when costs are more competitive, and services are more convenient.

SOURCE: Moroff, C (22 August 2018) "Seeing beyond size in vision care networks" (Web Blog Post). Retrieved from https://www.employeebenefitadviser.com/opinion/seeing-beyond-size-in-vision-care-networks?feed=00000152-a2fb-d118-ab57-b3ff6e310000

I Have Life Insurance Through My Employer. Why Do I Need Another Policy?

Life Happens in a Heartbeat - Stay Prepared With Saxon Life Insurance.

Although it is a subject no one wants to talk about, Life Insurance may be one of the best purchases you ever make.

Have you considered what would happen if you were not there to take care of your loved ones? Life insurance plans are about preparing for the unexpected. While nothing can replace you, having Life Insurance helps ensure that your family and loved ones would be financially stable if anything was to ever happen to you. Check out this article from Life Happens on the importance of obtaining Life Insurance - even if it's already offered through your employer.

One of the perks of having a full-time job with a good company is the benefits package that comes with it. Often, those benefits include life insurance coverage, which is great. And everyone who can get life insurance at work should definitely take it, as there are many advantages to company-funded life insurance, also known as group life insurance. These advantages include:

1. Easy qualification. Often, enrollment into group life insurance is automatic. That means everyone qualifies, as there is no medical exam required. So people who have preexisting health conditions, like diabetes or previous heart attack, can get life insurance at work, and may get a better rate compared with what an individual life insurance policy might cost them.

2. Lower costs. Employers’ insurance plans tend to be paid for or subsidized by the company, giving you life insurance at a low cost or even free. You may even have the option to buy additional coverage at low rates. Costs tend to be lower for many people because with group plans, the cost per individual goes down as the plan enlarges.

3. Convenience. It’s easy to subscribe to an employer’s life insurance plan without much effort on your part and if a payment is required, it’s easily deducted from your paycheck in much the same way as your medical costs are deducted.

These are all great advantages, but are these the only considerations that matter when it comes to life insurance? The answer, of course, is no.

Life insurance should first and foremost fit the purpose—it should meet your needs.

Life insurance should first and foremost fit the purpose—it should meet your needs. And the primary purpose of life insurance is to care for those left behind in the event of your death. With group life insurance, it’s often set at one or two times your annual salary, or a default amount such as $25,000 or $50,000. While this sounds like a lot of money, just think of how long that would last your loved ones. What would they do once that ran out?

There are several other disadvantages to relying on group insurance alone:

1. If your job situation changes, you’ll lose your coverage. Whether the change results from being laid off, moving from full-time to part-time status or leaving the job, in most cases, an employee can’t retain their policy when they leave their job.

2. Coverage may end when you retire or reach a specific age. Many people tend to lose their insurance coverage when they continue working past a specified age or when they retire. This means losing your insurance when you need it most.

3. Your employer can change or terminate the coverage. And that can be without your consent, since the contract is between your employer and the insurer.

4. Your options are limited. This type of coverage is not tailored to your specific needs. Furthermore, you may not be able to buy as much coverage as you need, leaving you exposed.

Importance of Buying a Separate Life Insurance Policy

It’s for these reasons you should get an individual life insurance policy that you personally own, in addition to any group life insurance you have. Individual life insurance plans offer superior benefits, and regardless of your employer or employment status, they remain in place and can be tailored to meet your needs and circumstances.

Most importantly, an individual life insurance policy will fit the purpose for which you purchase it—to ensure your dependents continue to have the financial means to keep their home and lifestyle in the unfortunate event that you’re no longer there to care for them.

Don't wait to protect your livelihood. Set up an appointment with one of our life insurance specialists here at Saxon by clicking this link.

Source:

Medina F. (19 June 2017). "I Have Life Insurance Through My Employer. Why Do I Need Another Policy?" [Web blog post]. Retrieved from address https://www.lifehappens.org/blog/i-have-life-insurance-through-my-employer-why-do-i-need-another-policy/

More than Half of Uninsured People Eligible for Marketplace Insurance Could Pay Less for Health Plan than Individual Mandate Penalty

Things are not looking up for the uninsured. Pay less and reach out to your health insurance professionals today. Want more facts? Check out this blog article from Kaiser Family Foundation.

A new Kaiser Family Foundation analysis finds that more than half (54% or 5.9 million) of the 10.7 million people who are uninsured and eligible to purchase an Affordable Care Act marketplace plan in 2018 could pay less in premiums for health insurance than they would owe as an individual mandate tax penalty for lacking coverage.

Within that 5.8 million, about 4.5 million (42% of the total) could obtain a bronze-level plan at no cost in 2018, after taking income-related premium tax credits into account, the analysis finds.

Most people without insurance who are eligible to buy marketplace coverage qualify for subsidies in the form of tax credits to help pay premiums for marketplace plans (8.3 million out of 10.7 million). Among those eligible for premium subsidies, the analysis finds that 70 percent could pay less in premiums than what they’d owe as a tax penalty for lacking coverage, with 54 percent able to purchase a bronze plan at no cost and 16 percent contributing less to their health insurance premium than the tax penalty they owe.

Among the 2.4 million uninsured, marketplace-eligible people who do not qualify for a premium subsidy, 2 percent would be able to pay less for marketplace insurance than they’d owe for their 2018 penalty, the analysis finds.

The Affordable Care Act’s individual mandate requires that most people have health coverage or be subject to a tax penalty unless they qualify for certain exemptions. The individual mandate is still in effect, though Congress may consider repealing it as part of tax legislation.

Consumers can compare their estimated 2018 individual mandate penalty with the cost of marketplace insurance in their area with KFF’s new Individual Mandate Penalty Calculator.

The deadline for ACA open enrollment in most states is Dec. 15, 2017.

You can read the original article here.

Source:

Kaiser Family Foundation (9 November 2017). "ANALYSIS: More than Half of Uninsured People Eligible for Marketplace Insurance Could Pay Less for Health Plan than Individual Mandate Penalty" [Web blog post]. Retrieved from address https://www.kff.org/health-reform/press-release/analysis-more-than-half-of-uninsured-people-eligible-for-marketplace-insurance-could-pay-less-for-health-plan-than-individual-mandate-penalty/

An Early Look at 2018 Premium Changes and Insurer Participation on ACA Exchanges

Each year insurers submit filings to state regulators detailing their plans to participate on the Affordable Care Act marketplaces (also called exchanges). These filings include information on the premiums insurers plan to charge in the coming year and which areas they plan to serve. Each state or the federal government reviews premiums to ensure they are accurate and justifiable before the rate goes into effect, though regulators have varying types of authority and states make varying amounts of information public.

In this analysis, we look at preliminary premiums and insurer participation in the 20 states and the District of Columbia where publicly available rate filings include enough detail to be able to show the premium for a specific enrollee. As in previous years, we focus on the second-lowest cost silver plan in the major city in each state. This plan serves as the benchmark for premium tax credits. Enrollees must also enroll in a silver plan to obtain reduced cost sharing tied to their incomes. About 71% of marketplace enrollees are in silver plans this year.

States are still reviewing premiums and participation, so the data in this report are preliminary and could very well change. Rates and participation are not locked in until late summer or early fall (insurers must sign an annual contract by September 27 in states using Healthcare.gov).

Insurers in this market face new uncertainty in the current political environment and in some cases have factored this into their premium increases for the coming year. Specifically, insurers have been unsure whether the individual mandate (which brings down premiums by compelling healthy people to buy coverage) will be repealed by Congress or to what degree it will be enforced by the Trump Administration. Additionally, insurers in this market do not know whether the Trump Administration will continue to make payments to compensate insurers for cost-sharing reductions (CSRs), which are the subject of a lawsuit, or whether Congress will appropriate these funds. (More on these subsidies can be found here).

The vast majority of insurers included in this analysis cite uncertainty surrounding the individual mandate and/or cost sharing subsidies as a factor in their 2018 rates filings. Some insurers explicitly factor this uncertainty into their initial premium requests, while other companies say if they do not receive more clarity or if cost-sharing payments stop, they plan to either refile with higher premiums or withdraw from the market. We include a table in this analysis highlighting examples of companies that have factored this uncertainty into their initial premium increases and specified the amount by which the uncertainty is increasing rates.

Changes in the Second-Lowest Cost Silver Premium

The second-lowest silver plan is one of the most popular plan choices on the marketplace and is also the benchmark that is used to determine the amount of financial assistance individuals and families receive. The table below shows these premiums for a major city in each state with available data. (Our analyses from 2017, 2016, 2015, and 2014 examined changes in premiums and participation in these states and major cities since the exchange markets opened nearly four years ago.)

Across these 21 major cities, based on preliminary 2018 rate filings, the second-lowest silver premium for a 40-year-old non-smoker will range from $244 in Detroit, MI to $631 in Wilmington, DE, before accounting for the tax credit that most enrollees in this market receive.

Of these major cities, the steepest proposed increases in the unsubsidized second-lowest silver plan are in Wilmington, DE (up 49% from $423 to $631 per month for a 40-year-old non-smoker), Albuquerque, NM (up 34% from $258 to $346), and Richmond, VA (up 33% from $296 to $394). Meanwhile, unsubsidized premiums for the second-lowest silver premiums will decrease in Providence, RI (down -5% from $261 to $248 for a 40-year-old non-smoker) and remain essentially unchanged in Burlington, VT ($492 to $491).

As discussed in more detail below, this year’s preliminary rate requests are subject to much more uncertainty than in past years. An additional factor driving rates this year is the return of the ACA’s health insurance tax, which adds an estimated 2 to 3 percentage points to premiums.

Most enrollees in the marketplaces (84%) receive a tax credit to lower their premium and these enrollees will be protected from premium increases, though they may need to switch plans in order to take full advantage of the tax credit. The premium tax credit caps how much a person or family must spend on the benchmark plan in their area at a certain percentage of their income. For this reason, in 2017, a single adult making $30,000 per year would pay about $207 per month for the second-lowest-silver plan, regardless of the sticker price (unless their unsubsidized premium was less than $207 per month). If this person enrolls in the second lowest-cost silver plan is in 2018 as well, he or she will pay slightly less (the after-tax credit payment for a similar person in 2018 will be $201 per month, or a decrease of 2.9%). Enrollees can use their tax credits in any marketplace plan. So, because tax credits rise with the increase in benchmark premiums, enrollees are cushioned from the effect of premium hikes.

| Table 1: Monthly Silver Premiums and Financial Assistance for a 40 Year Old Non-Smoker Making $30,000 / Year | ||||||||||

| State | Major City | 2nd Lowest Cost Silver Before Tax Credit |

2nd Lowest Cost Silver After Tax Credit |

Amount of Premium Tax Credit | ||||||

| 2017 | 2018 | % Change from 2017 |

2017 | 2018 | % Change from 2017 |

2017 | 2018 | % Change from 2017 |

||

| California* | Los Angeles | $258 | $289 | 12% | $207 | $201 | -3% | $51 | $88 | 71% |

| Colorado | Denver | $313 | $352 | 12% | $207 | $201 | -3% | $106 | $150 | 42% |

| Connecticut | Hartford | $369 | $417 | 13% | $207 | $201 | -3% | $162 | $216 | 33% |

| DC | Washington | $298 | $324 | 9% | $207 | $201 | -3% | $91 | $122 | 35% |

| Delaware | Wilmington | $423 | $631 | 49% | $207 | $201 | -3% | $216 | $430 | 99% |

| Georgia | Atlanta | $286 | $308 | 7% | $207 | $201 | -3% | $79 | $106 | 34% |

| Idaho | Boise | $348 | $442 | 27% | $207 | $201 | -3% | $141 | $241 | 70% |

| Indiana | Indianapolis | $286 | $337 | 18% | $207 | $201 | -3% | $79 | $135 | 72% |

| Maine | Portland | $341 | $397 | 17% | $207 | $201 | -3% | $134 | $196 | 46% |

| Maryland | Baltimore | $313 | $392 | 25% | $207 | $201 | -3% | $106 | $191 | 81% |

| Michigan* | Detroit | $237 | $244 | 3% | $207 | $201 | -3% | $29 | $42 | 44% |

| Minnesota** | Minneapolis | $366 | $383 | 5% | $207 | $201 | -3% | $159 | $181 | 14% |

| New Mexico | Albuquerque | $258 | $346 | 34% | $207 | $201 | -3% | $51 | $144 | 183% |

| New York*** | New York City | $456 | $504 | 10% | $207 | $201 | -3% | $249 | $303 | 21% |

| Oregon | Portland | $312 | $350 | 12% | $207 | $201 | -3% | $105 | $149 | 42% |

| Pennsylvania | Philadelphia | $418 | $515 | 23% | $207 | $201 | -3% | $211 | $313 | 49% |

| Rhode Island | Providence | $261 | $248 | -5% | $207 | $201 | -3% | $54 | $47 | -13% |

| Tennessee | Nashville | $419 | $507 | 21% | $207 | $201 | -3% | $212 | $306 | 44% |

| Vermont | Burlington | $492 | $491 | 0% | $207 | $201 | -3% | $285 | $289 | 2% |

| Virginia | Richmond | $296 | $394 | 33% | $207 | $201 | -3% | $89 | $193 | 117% |

| Washington | Seattle | $238 | $306 | 29% | $207 | $201 | -3% | $31 | $105 | 239% |

| NOTES: *The 2018 premiums for MI and CA reflect the assumption that CSR payments will continue. **The 2018 premium for MN assumes no reinsurance. ***Empire has filed to offer on the individual market in New York in 2018 but has not made its rates public. SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and insurer rate filings to state regulators. |

||||||||||

Looking back to 2014, when changes to the individual insurance market under the ACA first took effect, reveals a wide range of premium changes. In many of these cities, average annual premium growth over the 2014-2018 period has been modest, and in two cites (Indianapolis and Providence), benchmark premiums have actually decreased. In other cities, premiums have risen rapidly over the period, though in some cases this rapid growth was because premiums were initially quite low (e.g., in Nashville and Minneapolis).

| Table 2: Monthly Benchmark Silver Premiums for a 40 Year Old Non-Smoker, 2014-2018 |

||||||||

| State | Major City | 2014 | 2015 | 2016 | 2017 | 2018 | Average Annual % Change from 2014 to 2018 | Average Annual % Change After Tax Credit, $30K Income |

| California | Los Angeles | $255 | $257 | $245 | $258 | $289 | 3% | -1% |

| Colorado | Denver | $250 | $211 | $278 | $313 | $352 | 9% | -1% |

| Connecticut | Hartford | $328 | $312 | $318 | $369 | $417 | 6% | -1% |

| DC | Washington | $242 | $242 | $244 | $298 | $324 | 8% | -1% |

| Delaware | Wilmington | $289 | $301 | $356 | $423 | $631 | 22% | -1% |

| Georgia | Atlanta | $250 | $255 | $254 | $286 | $308 | 5% | -1% |

| Idaho | Boise | $231 | $210 | $273 | $348 | $442 | 18% | -1% |

| Indiana | Indianapolis | $341 | $329 | $298 | $286 | $337 | 0% | -1% |

| Maine | Portland | $295 | $282 | $288 | $341 | $397 | 8% | -1% |

| Maryland | Baltimore | $228 | $235 | $249 | $313 | $392 | 15% | -1% |

| Michigan* | Detroit | $224 | $230 | $226 | $237 | $244 | 2% | -1% |

| Minnesota** | Minneapolis | $162 | $183 | $235 | $366 | $383 | 24% | 6% |

| New Mexico | Albuquerque | $194 | $171 | $186 | $258 | $346 | 16% | 1% |

| New York*** | New York City | $365 | $372 | $369 | $456 | $504 | 8% | -1% |

| Oregon | Portland | $213 | $213 | $261 | $312 | $350 | 13% | -1% |

| Pennsylvania | Philadelphia | $300 | $268 | $276 | $418 | $515 | 14% | -1% |

| Rhode Island | Providence | $293 | $260 | $263 | $261 | $248 | -4% | -1% |

| Tennessee | Nashville | $188 | $203 | $281 | $419 | $507 | 28% | 2% |

| Vermont | Burlington | $413 | $436 | $468 | $492 | $491 | 4% | -1% |

| Virginia | Richmond | $253 | $260 | $276 | $296 | $394 | 12% | -1% |

| Washington | Seattle | $281 | $254 | $227 | $238 | $306 | 2% | -1% |

| NOTES: *The 2018 premiums for MI and CA reflect the assumption that CSR payments will continue. **The 2018 premium for MN assumes no reinsurance. ***Empire has filed to offer on the individual market in New York in 2018 but has not made its rates public. SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and insurer rate filings to state regulators. |

||||||||

Changes in Insurer Participation

Across these 20 states and DC, an average of 4.6 insurers have indicated they intend to participate in 2018, compared to an average of 5.1 insurers per state in 2017, 6.2 in 2016, 6.7 in 2015, and 5.7 in 2014. In states using Healthcare.gov, insurers have until September 27 to sign final contracts to participate in 2018. Insurers often do not serve an entire state, so the number of choices available to consumers in a particular area will typically be less than these figures.

| Table 3: Total Number of Insurers by State, 2014 – 2018 | |||||

| State | Total Number of Issuers in the Marketplace | ||||

| 2014 | 2015 | 2016 | 2017 | 2018 (Preliminary) | |

| California | 11 | 10 | 12 | 11 | 11 |

| Colorado | 10 | 10 | 8 | 7 | 7 |

| Connecticut | 3 | 4 | 4 | 2 | 2 |

| DC | 3 | 3 | 2 | 2 | 2 |

| Delaware | 2 | 2 | 2 | 2 | 1 (Aetna exiting) |

| Georgia | 5 | 9 | 8 | 5 | 4 (Humana exiting) |

| Idaho | 4 | 5 | 5 | 5 | 4 (Cambia exiting) |

| Indiana | 4 | 8 | 7 | 4 | 2 (Anthem and MDwise exiting) |

| Maine | 2 | 3 | 3 | 3 | 3 |

| Maryland | 4 | 5 | 5 | 3 | 3 (Cigna exiting, Evergreen1 filed to reenter) |

| Michigan | 9 | 13 | 11 | 9 | 8 (Humana exiting) |

| Minnesota | 5 | 4 | 4 | 4 | 4 |

| New Mexico | 4 | 5 | 4 | 4 | 4 |

| New York | 16 | 16 | 15 | 14 | 14 |

| Oregon | 11 | 10 | 10 | 6 | 5 (Atrio exiting) |

| Pennsylvania | 7 | 8 | 7 | 5 | 5 |

| Rhode Island | 2 | 3 | 3 | 2 | 2 |

| Tennessee | 4 | 5 | 4 | 3 | 3 (Humana exiting, Oscar entering) |

| Vermont | 2 | 2 | 2 | 2 | 2 |

| Virginia | 5 | 6 | 7 | 8 | 6 (UnitedHealthcare and Aetna exiting) |

| Washington | 7 | 9 | 8 | 6 | 5 (Community Health Plan of WA exiting) |

| Average (20 states + DC) | 5.7 | 6.7 | 6.2 | 5.1 | 4.6 |

| NOTES: Insurers are grouped by parent company or group affiliation, which we obtained from HHS Medical Loss Ratio public use files and supplemented with additional research. 1The number of preliminary 2018 insurers in Maryland includes Evergreen, which submitted a filing but has been placed in receivership. SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and insurer rate filings to state regulators. |

|||||

Uncertainty Surrounding ACA Provisions

Insurers in the individual market must submit filings with their premiums and service areas to states and/or the federal government for review well in advance of these rates going into effect. States vary in their deadlines and processes, but generally, insurers were required to submit their initial rate requests in May or June of 2017 for products that go into effect in January 2018. Once insurers set their premiums for 2018 and sign final contacts at the end of September, those premiums are locked in for the entire calendar year and insurers do not have an opportunity to revise their rates or service areas until the following year.

Meanwhile, over the course of this summer, the debate in Congress over repealing and replacing the Affordable Care Act has carried on as insurers set their rates for next year. Both the House and Senate bills included provisions that would have made significant changes to the law effective in 2018 or even retroactively, including repeal of the individual mandate penalty. Additionally, the Trump administration has sent mixed signals over whether it would continue to enforce the individual mandate or make payments to insurers to reimburse them for the cost of providing legally required cost-sharing assistance to low-income enrollees.

Because this policy uncertainty is far outside the norm, insurers are making varying assumptions about how this uncertainty will play out and affect premiums. Some states have attempted to standardize the process by requesting rate submissions under multiple scenarios, while other states appear to have left the decision up to each individual company. There is no standard place in the filings where insurers across all states can explain this type of assumption, and some states do not post complete filings to allow the public to examine which assumptions insurers are making.

In the 20 states and DC with detailed rate filings included in the previous sections of this analysis, the vast majority of insurers cite policy uncertainty in their rate filings. Some insurers make an explicit assumption about the individual mandate not being enforced or cost-sharing subsidies not being paid and specify how much each assumption contributes to the overall rate increase. Other insurers state that if they do not get clarity by the time final rates must be submitted – which has now been delayed to September 5 for the federal marketplace – they may either increase their premiums further or withdraw from the market.

Table 4 highlights examples of insurers that have explicitly factored into their premiums an assumption that either the individual mandate will not be enforced or cost-sharing subsidy payments will not be made and have specified the degree to which that assumption is influencing their initial rate request. As mentioned above, the vast majority of companies in states with detailed rate filings have included some language around the uncertainty, so it is likely that more companies will revise their premiums to reflect uncertainty in the absence of clear answers from Congress or the Administration.

Insurers assuming the individual mandate will not be enforced have factored in to their rate increases an additional 1.2% to 20%. Those assuming cost-sharing subsidy payments will not continue and factoring this into their initial rate requests have applied an additional rate increase ranging from 2% to 23%. Because cost-sharing reductions are only available in silver plans, insurers may seek to raise premiums just in those plans if the payments end. We estimate that silver premiums would have to increase by 19% on average to compensate for the loss of CSR payments, with the amount varying substantially by state.

Several insurers assumed in their initial rate filing that payment of the cost-sharing subsidies would continue, but indicated the degree to which rates would increase if they are discontinued. These insurers are not included in the Table 4. If CSR payments end or there is continued uncertainty, these insurers say they would raise their rates an additional 3% to 10% beyond their initial request – or ranging from 9% to 38% in cases when the rate increases would only apply to silver plans. Some states have instructed insurers to submit two sets of rates to account for the possibility of discontinued cost-sharing subsidies. In California, for example, a surcharge would be added to silver plans on the exchange, increasing proposed rates an additional 12.4% on average across all 11 carriers, ranging from 8% to 27%.

| Table 4: Examples of Preliminary Insurer Assumptions Regarding Individual Mandate Enforcement and Cost-Sharing Reduction (CSR) Payments |

|||||

| State | Insurer | Average Rate Increase Requested | Individual Mandate Assumption | CSR Payments Assumption | Requested Rate Increase Due to Mandate or CSR Uncertainty |

| CT | ConnectiCare | 17.5% | Weakly enforced1 | Not specified | Mandate: 2.4% |

| DE | Highmark BCBSD | 33.6% | Not enforced | Not paid | Mandate and CSR: 12.8% combined impact |

| GA | Alliant Health Plans | 34.5% | Not enforced | Not paid | Mandate: 5.0% CSR: Unspecified |

| ID | Mountain Health CO-OP | 25.0% | Not specified | Not paid | CSR: 17.0% |

| ID | PacificSource Health Plans | 45.6% | Not specified | Not paid | CSR: 23.2% |

| ID | SelectHealth | 45.0% | Not specified | Not paid | CSR: 20.0% |

| MD | CareFirst BlueChoice | 45.6% | Not enforced | Potentially not paid | Mandate: 20.0% |

| ME | Harvard PilgrimHealth Care | 39.7% | Weakly enforced | Potentially not paid | Mandate: 15.9% |

| MI | BCBS of MI | 26.9% | Weakly enforced | Potentially not paid (two rate submissions) | Mandate: 5.0% |

| MI | Blue Care Network of MI | 13.8% | Weakly enforced | Potentially not paid (two rate submissions) | Mandate: 5.0% |

| MI | Molina Healthcare of MI | 19.3% | Weakly enforced | Potentially not paid (two rate submissions) | Mandate: 9.5% |

| NM | CHRISTUS Health Plan | 49.2% | Not enforced | Potentially not paid | Mandate: 9.0%, combined impact of individual mandate non-enforcement and reduced advertising and outreach |

| NM | Molina Healthcare of NM | 21.2% | Weakly enforced | Paid | Mandate: 11.0% |

| NM | New Mexico Health Connections | 32.8% | Not enforced | Potentially not paid | Mandate: 20.0% |

| OR* | BridgeSpan | 17.2% | Weakly enforced | Potentially not paid | Mandate: 11.0% |

| OR* | Moda Health | 13.1% | Not enforced | Potentially not paid | Mandate: 1.2% |

| OR* | Providence Health Plan | 20.7% | Not enforced | Potentially not paid | Mandate: 9.7%, largely due to individual mandate non-enforcement |

| TN | BCBS of TN | 21.4% | Not enforced | Not paid | Mandate: 7.0% CSR: 14.0% |

| TN | Cigna | 42.1% | Weakly enforced | Not paid | CSR: 14.1% |

| TN | Oscar Insurance | NA (New to state) | Not enforced | Not paid | Mandate: 0%, despite non-enforcement CSR: 17.0%, applied only to silver plans |

| VA | CareFirst BlueChoice | 21.5% | Not enforced | Potentially not paid | Mandate: 20.0% |

| VA | CareFirst GHMSI | 54.3% | Not enforced | Potentially not paid | Mandate: 20.0% |

| WA | LifeWise Health Plan of Washington | 21.6% | Weakly enforced | Not paid | Mandate: 5.2% CSR: 2.3% |

| WA | Premera Blue Cross | 27.7% | Weakly enforced | Not paid | Mandate: 4.0% CSR: 3.1% |

| WA | Molina Healthcare of WA | 38.5% | Weakly enforced | Paid | Mandate: 5.4% |

| NOTES: The CSR assumption “Potentially not paid” refers to insurers that filed initial rates assuming CSR payments are made and indicated that uncertainty over CSR funding would change their initial rate requests. In Michigan, insurers were instructed to submit a second set of filings showing rate increases without CSR payments; the rates shown above assume continued CSR payments. *The Oregon Division of Financial Regulation reviewed insurer filings and advised adjustment of the impact of individual mandate uncertainty to between 2.4% and 5.1%. Although rates have since been finalized, the increases shown here are based on initial insurer requests. 1Connecticare assumes a public perception that the mandate will not be enforced. SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and insurer rate filings to state regulators. |

|||||

Discussion

A number of insurers have requested double-digit premium increases for 2018. Based on initial filings, the change in benchmark silver premiums will likely range from -5% to 49% across these 21 major cities. These rates are still being reviewed by regulators and may change.

In the past, requested premiums have been similar, if not equal to, the rates insurers ultimately charge. This year, because of the uncertainty insurers face over whether the individual mandate will be enforced or cost-sharing subsidy payments will be made, some companies have included an additional rate increase in their initial rate requests, while other companies have said they may revise their premiums late in the process. It is therefore quite possible that the requested rates in this analysis will change between now and open enrollment.

Insurers attempting to price their plans and determine which states and counties they will service next year face a great deal of uncertainty. They must soon sign contracts locking in their premiums for the entire year of 2018, yet Congress or the Administration could make significant changes in the coming months to the law – or its implementation – that could lead to significant losses if companies have not appropriately priced for these changes. Insurers vary in the assumptions they make regarding the individual mandate and cost-sharing subsidies and the degree to which they are factoring this uncertainty into their rate requests.

Because most enrollees on the exchange receive subsidies, they will generally be protected from premium increases. Ultimately, most of the burden of higher premiums on exchanges falls on taxpayers. Middle and upper-middle income people purchasing their own coverage off-exchange, however, are not protected by subsidies and will pay the full premium increase, switch to a lower level plan, or drop their coverage. Although the individual market on average has been stabilizing, the concern remains that another year of steep premium increases could cause healthy people (particularly those buying off-exchange) to drop their coverage, potentially leading to further rate hikes or insurer exits.

Methods

Data were collected from health insurer rate filing submitted to state regulators. These submissions are publicly available for the states we analyzed. Most rate information is available in the form of a SERFF filing (System for Electronic Rate and Form Filing) that includes a base rate and other factors that build up to an individual rate. In states where filings were unavailable, we gathered data from tables released by state insurance departments. Premium data are current as of August 7, 2017; however, filings in most states are still preliminary and will likely change before open enrollment. All premiums in this analysis are at the rating area level, and some plans may not be available in all cities or counties within the rating area. Rating areas are typically groups of neighboring counties, so a major city in the area was chosen for identification purposes.

CenterStage...Open Season for Open Enrollment

In this month’s CenterStage, we interviewed Rich Arnold for some in-depth information on Medicare plans and health coverage. Read the full article below.

Open Season for Open Enrollment: What does it mean for you?

There are 10,000 people turning 65 every single day. Medicare has a lot of options, causing the process to be extremely confusing. Rich – a Senior Solutions Advisor – works hard to provide you with the various options available to seniors in Ohio, Kentucky and Indiana and reduce them to an ideal, simple, and easy-to-follow plan.

“For me, this is all about helping people.”

– Rich Arnold, Senior Solutions Advisor

What does this call for?

To provide clients with top-notch Medicare guidance, Rich must analyze their current doctors and drugs for the best plan option and properly educate them to choose the best program for their situation and health. It’s a simple, free process of evaluation, education, and enrollment.

For this month’s CenterStage article, we asked Rich to break down Medicare for the senior population who are in desperate need of a break from the confusion.

Medicare Break Down

Part A. Hospitalization, Skilled Nursing, etc.

If you’ve worked for 40 quarters, you automatically obtain Part A coverage.

Part B. Medical Services: Doctors, Surgeries, Outpatient visits, etc.…

You must enroll and pay a monthly premium.

Part C. Medicare Advantage Plans:

Provides most of your hospital and medical expenses.

Part D.

Prescription drug plans available with Medicare.

Under Parts A & B there are two types of plans…

Supplement Plan or Medigap Plan

A Medicare Supplement Insurance (Medigap) policy can help pay some of the health care costs that Original Medicare doesn’t cover, like copayments, coinsurance, and deductibles, coverage anywhere in the US as well as travel outside of the country, pay a monthly amount, and usually coupled with a prescription drug plan.

Advantage Plan

A type of Medicare health plan that contracts with Medicare to provide you with all your Part A and Part B benefits generally through a HMO or PPO, pay a monthly amount from $0 and up, covers emergency services, and offers prescription drug plans.

How does this effect you?

Medicare starts at 65 years of age, but Rich advises anyone turning 63 or 64 years of age to reach out to an advisor, such as himself, for zero cost, to be put onto their calendar to follow up at the proper time to investigate the Medicare options. Some confusion exists about Medicare and Social Security which are separate entities. Social Security does not pay for the Supplement or Advantage plans.

Medicare Open Enrollment: Open Enrollment occurs between October 15th and December 7 – yes, right around the corner! However, don’t panic, Rich and his services can help you if you are turning 65 or if you haven’t reviewed your current plan in over a year – you should seek his guidance.

Your plan needs to be reviewed every year to best fit your needs. If you’re on the verge of 65, turning 65 in the next few months, or over 65, you should consult your Medicare advisor as soon as possible. For a no cost analysis of your needs contact Rich, Saxon Senior Solutions Advisor, rarnold@gosaxon.com, 513-808-4879.

The Medicare Part D Prescription Drug Benefit

Below we have an article from the Kaiser Family Foundation providing detailed information and graphics on the benefit of the Medicare Prescription Drug Plan.

You can read the original article here.

Medicare Part D is a voluntary outpatient prescription drug benefit for people on Medicare that went into effect in 2006. All 59 million people on Medicare, including those ages 65 and older and those under age 65 with permanent disabilities, have access to the Part D drug benefit through private plans approved by the federal government; in 2017, more than 42 million Medicare beneficiaries are enrolled in Medicare Part D plans. During the Medicare Part D open enrollment period, which runs from October 15 to December 7 each year, beneficiaries can choose to enroll in either stand-alone prescription drug plans (PDPs) to supplement traditional Medicare or Medicare Advantage prescription drug (MA-PD) plans (mainly HMOs and PPOs) that cover all Medicare benefits including drugs. Beneficiaries with low incomes and modest assets are eligible for assistance with Part D plan premiums and cost sharing. This fact sheet provides an overview of the Medicare Part D program and information about 2018 plan offerings, based on data from the Centers for Medicare & Medicaid Services (CMS) and other sources.

Medicare Prescription Drug Plan Availability in 2018

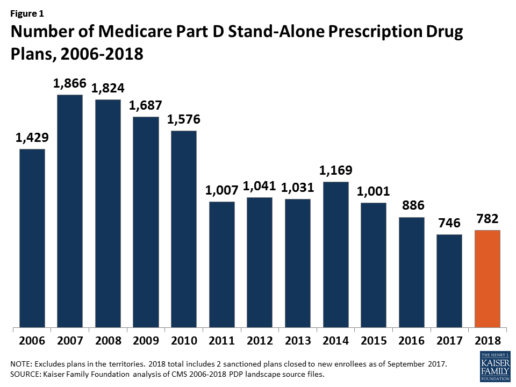

In 2018, 782 PDPs will be offered across the 34 PDP regions nationwide (excluding the territories). This represents an increase of 36 PDPs, or 5%, since 2017, but a reduction of 104 plans, or 12%, since 2016 (Figure 1).

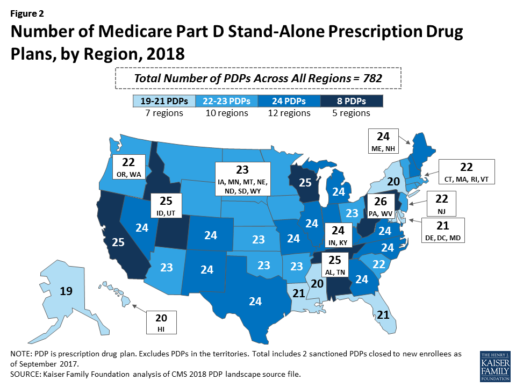

Beneficiaries in each state will continue to have a choice of multiple stand-alone PDPs in 2018, ranging from 19 PDPs in Alaska to 26 PDPs in Pennsylvania/West Virginia (in addition to multiple MA-PD plans offered at the local level) (Figure 2).

Low-Income Subsidy Plan Availability in 2018

Through the Part D Low-Income Subsidy (LIS) program, additional premium and cost-sharing assistance is available for Part D enrollees with low incomes (less than 150% of poverty, or $18,090 for individuals/$24,360 for married couples in 2017) and modest assets (less than $13,820 for individuals/$27,600 for couples in 2017).1

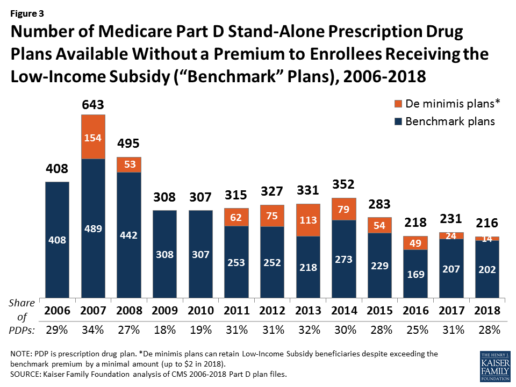

In 2018, 216 plans will be available for enrollment of LIS beneficiaries for no premium, a 6% decrease in premium-free (“benchmark”) plans from 2017 and the lowest number of benchmark plans available since the start of the Part D program in 2006. Roughly 3 in 10 PDPs in 2018 (28%) are benchmark plans (Figure 3).

Low-Income Subsidy Plan Availability in 2018

Through the Part D Low-Income Subsidy (LIS) program, additional premium and cost-sharing assistance is available for Part D enrollees with low incomes (less than 150% of poverty, or $18,090 for individuals/$24,360 for married couples in 2017) and modest assets (less than $13,820 for individuals/$27,600 for couples in 2017).1

In 2018, 216 plans will be available for enrollment of LIS beneficiaries for no premium, a 6% decrease in premium-free (“benchmark”) plans from 2017 and the lowest number of benchmark plans available since the start of the Part D program in 2006. Roughly 3 in 10 PDPs in 2018 (28%) are benchmark plans (Figure 3).

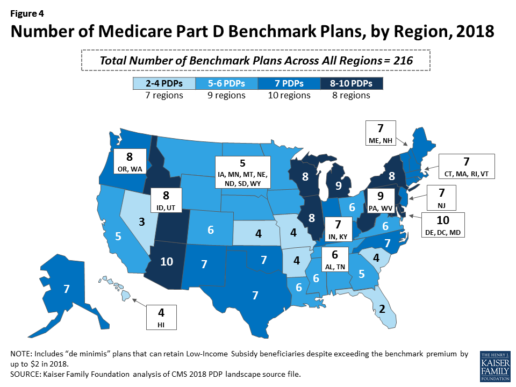

Benchmark plan availability varies at the Part D region level, with most regions seeing a reduction of 1 benchmark plan for 2018 (Figure 4). The number of premium-free plans in 2018 ranges from a low of 2 plans in Florida to 10 plans in Arizona and Delaware/Maryland/Washington D.C.

Part D Plan Premiums and Benefits in 2018

Premiums. According to CMS, the 2018 Part D base beneficiary premium is $35.02, a modest decline of 2% from 2017.2 Actual (unweighted) PDP monthly premiums for 2018 vary across plans and regions, ranging from a low of $12.60 for a PDP available in 12 out of 34 regions to a high of $197 for a PDP in Texas.

Part D enrollees with higher incomes ($85,000/individual; $170,000/couple) pay an income-related monthly premium surcharge, ranging from $13.00 to $74.80 in 2018 (depending on their income level), in addition to the monthly premium for their specific plan.3 According to CMS projections, an estimated 3.3 million Part D enrollees (7%) will pay income-related Part D premiums in 2018.

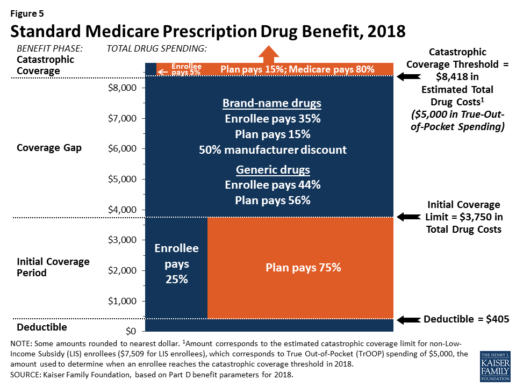

Benefits. In 2018, the Part D standard benefit has a $405 deductible and 25% coinsurance up to an initial coverage limit of $3,750 in total drug costs, followed by a coverage gap. During the gap, enrollees are responsible for a larger share of their total drug costs than in the initial coverage period, until their total out-of-pocket spending in 2018 reaches $5,000 (Figure 5).

After enrollees reach the catastrophic coverage threshold, Medicare pays for most (80%) of their drug costs, plans pay 15%, and enrollees pay either 5% of total drug costs or $3.35/$8.35 for each generic and brand-name drug, respectively.

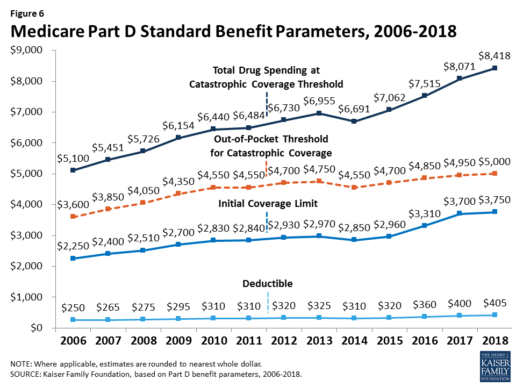

The standard benefit amounts are indexed to change annually by rate of Part D per capita spending growth, and, with the exception of 2014, have increased each year since 2006 (Figure 6).

Part D plans must offer either the defined standard benefit or an alternative equal in value (“actuarially equivalent”), and can also provide enhanced benefits. But plans can (and do) vary in terms of their specific benefit design, cost-sharing amounts, utilization management tools (i.e., prior authorization, quantity limits, and step therapy), and formularies (i.e., covered drugs). Plan formularies must include drug classes covering all disease states, and a minimum of two chemically distinct drugs in each class. Part D plans are required to cover all drugs in six so-called “protected” classes: immunosuppressants, antidepressants, antipsychotics, anticonvulsants, antiretrovirals, and antineoplastics.

In 2018, almost half (46%) of plans will offer basic Part D benefits (although no plans will offer the defined standard benefit), while 54% will offer enhanced benefits, similar to 2017. Most PDPs (63%) will charge a deductible, with 52% of all PDPs charging the full amount ($405). Most plans have shifted to charging tiered copayments or varying coinsurance amounts for covered drugs rather than a uniform 25% coinsurance rate, and a substantial majority of PDPs use specialty tiers for high-cost medications. Two-thirds of PDPs (65%) will not offer additional gap coverage in 2018 beyond what is required under the standard benefit. Additional gap coverage, when offered, has been typically limited to generic drugs only (not brands).

The 2010 Affordable Care Act gradually lowers out-of-pocket costs in the coverage gap by providing enrollees with a 50% manufacturer discount on the total cost of their brand-name drugs filled in the gap and additional plan payments for brands and generics. In 2018, Part D enrollees in plans with no additional gap coverage will pay 35% of the total cost of brands and 44% of the total cost of generics in the gap until they reach the catastrophic coverage threshold. Medicare will phase in additional subsidies for brands and generic drugs, ultimately reducing the beneficiary coinsurance rate in the gap to 25% by 2020.

Part D and Low-Income Subsidy Enrollment

Enrollment in Medicare drug plans is voluntary, with the exception of beneficiaries who are dually eligible for both Medicare and Medicaid and certain other low-income beneficiaries who are automatically enrolled in a PDP if they do not choose a plan on their own. Unless beneficiaries have drug coverage from another source that is at least as good as standard Part D coverage (“creditable coverage”), they face a penalty equal to 1% of the national average premium for each month they delay enrollment.

In 2017, more than 42 million Medicare beneficiaries are enrolled in Medicare Part D plans, including employer-only group plans.4 Of this total, 6 in 10 (60%) are enrolled in stand-alone PDPs and 4 in 10 (40%) are enrolled in Medicare Advantage drug plans. Medicare’s actuaries estimate that around 2 million other beneficiaries in 2017 have drug coverage through employer-sponsored retiree plans where the employer receives subsidies equal to 28% of drug expenses between $405 and $8,350 per retiree in 2018 (up from $400 and $8,250 in 2017).5 Several million beneficiaries are estimated to have other sources of drug coverage, including employer plans for active workers, FEHBP, TRICARE, and Veterans Affairs (VA). Yet an estimated 12% of Medicare beneficiaries lack creditable drug coverage.

Twelve million Part D enrollees are currently receiving the Low-Income Subsidy. Beneficiaries who are dually eligible, QMBs, SLMBs, QIs, and SSI-onlys automatically qualify for the additional assistance, and Medicare automatically enrolls them into PDPs with premiums at or below the regional average (the Low-Income Subsidy benchmark) if they do not choose a plan on their own. Other beneficiaries are subject to both an income and asset test and need to apply for the Low-Income Subsidy through either the Social Security Administration or Medicaid.

Part D Spending and Financing in 2018

The Congressional Budget Office (CBO) estimates that spending on Part D benefits will total $92 billion in 2018, representing 15.5% of net Medicare outlays in 2018 (net of offsetting receipts from premiums and state transfers). Part D spending depends on several factors, including the number of Part D enrollees, their health status and drug use, the number of enrollees receiving the Low-Income Subsidy, and plans’ ability to negotiate discounts (rebates) with drug companies and preferred pricing arrangements with pharmacies, and manage use (e.g., promoting use of generic drugs, prior authorization, step therapy, quantity limits, and mail order). Federal law prohibits the Secretary of Health and Human Services from interfering in drug price negotiations between Part D plan sponsors and drug manufacturers.6

Financing for Part D comes from general revenues (78%), beneficiary premiums (13%), and state contributions (9%). The monthly premium paid by enrollees is set to cover 25.5% of the cost of standard drug coverage. Medicare subsidizes the remaining 74.5%, based on bids submitted by plans for their expected benefit payments. Part D enrollees with higher incomes ($85,000/individual; $170,000/couple) pay a greater share of standard Part D costs, ranging from 35% to 80%, depending on income.

According to Medicare’s actuaries, in 2018, Part D plans are projected to receive average annual direct subsidy payments of $353 per enrollee overall and $2,353 for enrollees receiving the LIS; employers are expected to receive, on average, $623 for retirees in employer-subsidy plans.7 Part D plans’ potential total losses or gains are limited by risk-sharing arrangements with the federal government (“risk corridors”). Plans also receive additional risk-adjusted payments based on the health status of their enrollees and reinsurance payments for very high-cost enrollees.

Under reinsurance, Medicare subsidizes 80% of drug spending incurred by Part D enrollees above the catastrophic coverage threshold. In 2018, average reinsurance payments per enrollee are estimated to be $941; this represents a 7% increase from 2017. Medicare’s reinsurance payments to plans have represented a growing share of total Part D spending, increasing from 16% in 2007 to an estimated 41% in 2018.8 This is due in part to a growing number of Part D enrollees with spending above the catastrophic threshold, resulting from several factors, including the introduction of high-cost specialty drugs, increases in the cost of prescriptions, and a change made by the ACA to count the 50% manufacturer discount in enrollees’ out-of-pocket spending that qualifies them for catastrophic coverage. Analysis from MedPAC also suggests that in recent years, plans have underestimated their enrollees’ expected costs above the catastrophic coverage threshold, resulting in higher reinsurance payments from Medicare to plans over time.

Issues for the Future

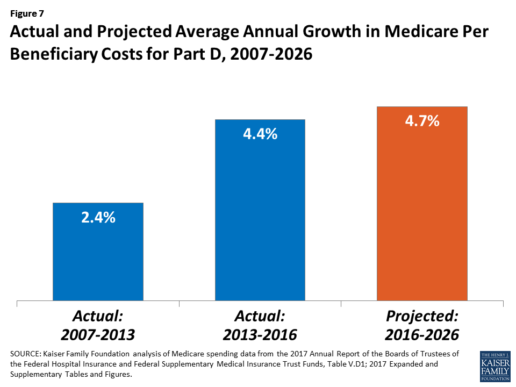

After several years of relatively low growth in prescription drug spending, spending has risen more steeply since 2013. The average annual rate of growth in Part D costs per beneficiary was 2.4% between 2007 and 2013, but it increased to 4.4% between 2013 and 2016, and is projected to increase by 4.7% between 2016 and 2026

(Figure 7).9

Medicare’s actuaries have projected that the Part D per capita growth rate will be comparatively higher in the coming years than in the program’s initial years due to higher costs associated with expensive specialty drugs, which is expected to be reflected in higher reinsurance payments to plans. Between 2017 and 2027, spending on Part D benefits is projected to increase from 15.9% to 17.5% of total Medicare spending (net of offsetting receipts).10 Understanding whether and to what extent private plans are able to negotiate price discounts and rebates will be an important part of ongoing efforts to assess how well plans are able to contain rising drug costs. However, drug-specific rebate information is not disclosed by CMS.

The Medicare drug benefit helps to reduce out-of-pocket drug spending for enrollees, which is especially important to those with modest incomes or very high drug costs. Closing the coverage gap by 2020 will bring additional relief to millions of enrollees with high costs. But with drug spending on the rise and more plans charging coinsurance rather than flat copayments for covered brand-name drugs, enrollees could face higher out-of-pocket costs for their Part D coverage. These trends highlight the importance of comparing plans during the annual enrollment period. Research shows, however, that relatively few people on Medicare have used the annual opportunity to switch Part D plans voluntarily—even though those who do switch often lower their out-of-pocket costs as a result of changing plans.

Understanding how well Part D is working and how well it is meeting the needs of people on Medicare will be informed by ongoing monitoring of the Part D plan marketplace and plan enrollment; assessing coverage and costs for high-cost biologics and other specialty drugs; exploring the relationship between Part D spending and spending on other Medicare-covered services; and evaluating the impact of the drug benefit on Medicare beneficiaries’ out-of-pocket spending and health outcomes.

Endnotes

- Poverty and resource levels for 2018 are not yet available (as of September 2017).

- The base beneficiary premium is equal to the product of the beneficiary premium percentage and the national average monthly bid amount (which is an enrollment-weighted average of bids submitted by both PDPs and MA-PD plans). Centers for Medicare & Medicaid Services, “Annual Release of Part D National Average Bid Amount and Other Part C & D Bid Information,” July 31, 2017, available at https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/PartDandMABenchmarks2018.pdf.

- Higher-income Part D enrollees also pay higher monthly Part B premiums.

- Centers for Medicare & Medicaid Services, Medicare Advantage, Cost, PACE, Demo, and Prescription Drug Plan Contract Report – Monthly Summary Report (Data as of August 2017).

- Board of Trustees, 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds, Table IV.B7, available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2017.pdf.

- Social Security Act, Section 1860D-11(i).

- 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds; Table IV.B9.

- Kaiser Family Foundation analysis of aggregate Part D reimbursement amounts from Table IV.B10, 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.

- Kaiser Family Foundation analysis of Part D average per beneficiary costs from Table V.D1, 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.

- Kaiser Family Foundation analysis of Part D benefits spending as a share of net Medicare outlays (total mandatory and discretionary outlays minus offsetting receipts) from CBO, Medicare-Congressional Budget Office’s June 2017 Baseline.

Read the full article here.

Source:

Kaiser Family Foundation (2 October 2017). “The Medicare Part D Prescription Drug Benefit” [Web Blog Post]. Retrieved from address https://www.kff.org/medicare/fact-sheet/the-medicare-prescription-drug-benefit-fact-sheet/#26740

Health Law Sleepers: Six Surprising Health Items That Could Disappear With ACA Repeal

Does ACA repeal have you worried? Look into this great article from Kaiser Health News about some of things that could disappear with ACA repeal by Julie Appleby and Mary Agnes Carey

The Affordable Care Act of course affected premiums and insurance purchasing. It guaranteed people with pre-existing conditions could buy health coverage and allowed children to stay on parents’ plans until age 26. But the roughly 2,000-page bill also included a host of other provisions that affect the health-related choices of nearly every American.

Some of these measures are evident every day. Some enjoy broad support, even though people often don’t always realize they spring from the statute.

In other words, the outcome of the repeal-and-replace debate could affect more than you might think, depending on exactly how the GOP congressional majority pursues its goal to do away with Obamacare.

No one knows how far the effort will reach, but here’s a sampling of sleeper provisions that could land on the cutting-room floor:

CALORIE COUNTS AT RESTAURANTS AND FAST FOOD CHAINS

Feeling hungry? The law tries to give you more information about what that burger or muffin will cost you in terms of calories, part of an effort to combat the ongoing obesity epidemic. Under the ACA, most restaurants and fast food chains with at least 20 stores must post calorie counts of their menu items. Several states, including New York, already had similar rules before the law. Although there was some pushback, the rule had industry support, possibly because posting calories was seen as less onerous than such things as taxes on sugary foods or beverages. The final rule went into effect in December after a one-year delay. One thing that is still unclear: Does simply seeing that a particular muffin has more than 400 calories cause consumers to choose carrot sticks instead? Results are mixed. One large meta-analysis done before the law went into effect didn’t show a significant reduction in calorie consumption, although the authors concluded that menu labeling is “a relatively low-cost education strategy that may lead consumers to purchase slightly fewer calories.”

PRIVACY PLEASE: WORKPLACE REQUIREMENTS FOR BREAST-FEEDING ROOMS

Breast feeding, but going back to work? The law requires employers to provide women break time to express milk for up to a year after giving birth and provide someplace — other than a bathroom — to do so in private. In addition, most health plans must offerbreastfeeding support and equipment, such as pumps, without a patient co-payment.

LIMITS ON SURPRISE MEDICAL COSTS FROM HOSPITAL EMERGENCY ROOM VISITS

If you find yourself in an emergency room, short on cash, uninsured or not sure if your insurance covers costs at that hospital, the law provides some limited assistance. If you are in a hospital that is not part of your insurer’s network, the Affordable Care Act requires all health plans to charge consumers the same co-payments or co-insurance for out-of-network emergency care as they do for hospitals within their networks. Still, the hospital could “balance bill” you for its costs — including ER care — that exceed what your insurer reimburses it.

If it’s a non-profit hospital — and about 78 percent of all hospitals are — the law requires it to post online a written financial assistance policy, spelling out whether it offers free or discounted care and the eligibility requirements for such programs. While not prescribing any particular set of eligibility requirements, the law requires hospitals to charge lower rates to patients who are eligible for their financial assistance programs. That’s compared with their gross charges, also known as chargemaster rates.

NONPROFIT HOSPITALS’ COMMUNITY HEALTH ASSESSMENTS

The health law also requires non-profit hospitals to justify the billions of dollars in tax exemptions they receive by demonstrating how they go about trying to improve the health of the community around them.

Every three years, these hospitals have to perform a community needs assessment for the area the hospital serves. They also have to develop — and update annually — strategies to meet these needs. The hospitals then must provide documentation as part of their annual reporting to the Internal Revenue Service. Failure to comply could leave them liable for a $50,000 penalty.

A WOMAN’S RIGHT TO CHOOSE … HER OB/GYN

Most insurance plans must allow women to seek care from an obstetrician/gynecologist without having to get a referral from a primary care physician. While the majority of states already had such protections in place, those laws did not apply to self-insured plans, which are often offered by large employers. The health law extended the rules to all new plans. Proponents say direct access makes it easier for women to seek not only reproductive health care, but also related screenings for such things as high blood pressure or cholesterol.

AND WHAT ABOUT THOSE THERAPY COVERAGE ASSURANCES FOR FAMILIES WHO HAVE KIDS WITH AUTISM?

Advocates for children with autism and people with degenerative diseases argued that many insurance plans did not provide care their families needed. That’s because insurers would cover rehabilitation to help people regain functions they had lost, such as walking again after a stroke, but not care needed to either gain functions patients never had, such speech therapy for a child who never learned how to talk, or to maintain a patient’s current level of function. The law requires plans to offer coverage for such treatments, dubbed habilitative care, as part of the essential health benefits in plans sold to individuals and small groups.

See the original article Here.

Source:

Appleby J., Carey M. (2017 January 12). Health law sleepers: six surprising health items that could disappear with ACA repeal [Web blog post]. Retrieved from address https://khn.org/news/health-law-sleepers-six-surprising-health-items-that-could-disappear-with-aca-repeal/?utm_campaign=KHN%3A+Daily+Health+Policy+Report&utm_source=hs_email&utm_medium=email&utm_content=40532225&_hsenc=p2ANqtz-8vl0H_K8CNgaURbqgYS5m3isu1NUGrj0FRIdsUX8JCwcifTDRV-UvKdu6lZGvB06FTyhENvPFLaOMOsIrr2IBVBTNWQg&_hsmi=40532225

Health insurers willing to give up a key ACA provision

Great article about new changes to the ACA from BenefitsPro by Zachary Tracer

U.S. health insurers signaled Tuesday that they’re willing to give up a cornerstone provision of Obamacare that requires all Americans to have insurance, replacing it with a different set of incentives less loathed by Republicans who have promised to repeal the law.

Known as the “individual mandate,” the rule was a major priority for the insurance industry when the Affordable Care Act was legislated, and also became a focal point of opposition for Republicans.

In a position paper released Tuesday -- the first since President-elect Donald Trump’s victory -- health insurers laid out changes they’d be willing to accept.

“Replacing the individual mandate with strong, effective incentives, such as late enrollment penalties and waiting periods, can help expand coverage and lower costs for everyone,” AHIP said.

That also includes openness to Republican ideas such as an expanded role for health-savings accounts and using so-called high-risk pools to cover sick people.

In return, insurers are asking Republicans to create strong incentives to buy insurance, and to ensure the government continues to make good on payments it owes insurers under the ACA. The paper was released by America’s Health Insurance Plans, or AHIP, the main lobby for the industry.

“Millions of Americans depend on their current care and coverage,” AHIP said in the document outlining its positions. The group called on lawmakers to “ensure that people’s coverage -- and lives -- are not disrupted.”

Republican replacement

Now that they’re set to gain control of the White House, Republican lawmakers are working to define their vision for replacing the law after years of attempts to repeal it. Obamacare brought insurance coverage to about 20 million people via an expansion of Medicaid and new insurance markets, and repealing the law without a replacement would leave those individuals without coverage.

Trump has said that repealing and then replacing the law will be one of his first priorities. Republicans in Congress, however, have signaled that they’ll need time to write a replacement -- potentially via a years-long delay between passing a repeal and implementing it -- to craft a replacement.

And AHIP on Thursday said insurers will need at least 18 months to create new products and get them approved by state regulators, if Republicans change the market. It could take even more time to educate consumers and change state laws, AHIP said.

“It’s taken six years to get where we are now and to demonstrate the failure of Obamacare, so it’s going to take us a little while to fix it,” said Senator John Cornyn of Texas, a member of the Republican leadership in the chamber.

Medicaid changes

Republicans may also make substantial changes to Medicaid, by turning the joint state-federal program into one where the U.S. sends “block grants” to the states, which exert more control. Vice President-elect Mike Pence said on CNN Tuesday that the Trump administration will “develop a plan to block-grant Medicaid back to the states” so they can reform the program. Some Medicaid programs are administered in part by private insurers.

AHIP said any such plans should ensure that payments are adequate to meet the health needs of individuals in Medicaid coverage. And they should ensure that when enrollment increases in an economic downturn, funds are available to help states deal with the increased demand, AHIP said.

AHIP is open to working with Congress on replacement plans for the ACA, said Kristine Grow, a spokeswoman for the lobby group. The document is the first detailed look at AHIP’s priorities.

Big insurers like UnitedHealth Group Inc. and Aetna Inc. are already scaling back from the ACA’s markets, because they’re losing money. At the same time, remaining insurers are boosting premiums by more than 20 percent on average for next year.

Trump’s election increased the level of uncertainty in the market, and a repeal bill without something to replace the law could destabilize it further. To shore up insurance markets, AHIP says lawmakers should fund a program, known as reinsurance, designed to help insurers with high costs, through the end of 2018, and avoid cutting off cost-sharing subsidies for low-income individuals.

See the original article Here.

Source:

Tracer Z.(2016 December 7). Health insurers willing to give up a key ACA provision[Web blog post]. Retrieved from address https://www.benefitspro.com/2016/12/07/health-insurers-willing-to-give-up-a-key-aca-provi?ref=mostpopular&page_all=1