Simple Open-Enrollment Tips That Can Make a Big Difference

Many employees associate fear, anxiety or apprehension with open enrollment, the annual period when they select which employer-sponsored benefits they will have the coming year. Read this blog post from SHRM For a few simple tips to help out with this open enrollment season.

Trepidation is what comes to mind for many employees when asked their feelings about open enrollment, the annual period when they select employer-provided benefits for the coming year.

According to a nationally representative sample of 1,000 employees polled earlier this year, 33 percent cited "annoyance" or "dread" as their primary emotions when they thought about open enrollment and just 10 percent of workers said they were "confident" in the benefits choices they made when the enrollment process was over, according to VSP Vision Care's annual Open Talk about Open Enrollment survey.

In another survey, HR software company Namely found that 31 percent of employees give their employer a "C" or lower when it comes to open enrollment.

Here are some tips from benefits experts that will help you raise your grade this open-enrollment season.

What to Do, and Not to Do

Jennifer Benz, national practice leader at benefits communications firm Segal Benz, shared three bad HR practices that undermine open enrollment and three best practices for doing open enrollment the right way.

- Don't hide vital information from employees. Benz recalls how one company sent out its benefits materials but didn't include monthly costs. "A group of enterprising employees crunched the numbers and came up with estimates and circulated a rogue spreadsheet. Dealing with this communications fiasco took more work" than being upfront about costs, she noted.

Best practice: Be transparent and share the reasons you are making benefits changes. Break down the details and do the work for the employees. Provide scenarios so employees can better understand their options and cost breakdowns for different life situations.

- Don't cram in every benefit at once. Some companies hand out pages and pages of text, jamming a year's worth of communications into a few weeks, and figure they have done what they need to do. "What they have done is confused their employees," Benz said.

Best practices: Communicate the technical details of your various benefits over time. "Don't assume employees will weed through all your materials to make sense of the benefits offered to them," Benz said. Also make full use of visual aids. "Photos, icons, infographics, memes, charts, graphics and more—they all help to attract, and more importantly hold, people's attention," noted Amber Riley, a communications consultant to Segal Benz. "Whether you're driving an open-enrollment campaign, creating a new benefits guide or promoting a wellness program, when you increase the visual pleasure of what you are communicating, your people are more likely to engage, learn, understand and ultimately take action."

- Don't give employees too little time to process their open-enrollment choices. While many people wait until the last day to fill out the health care selection forms, they may have been considering their options with family members for weeks, so giving them just a few days to make decisions is not going to be enough.

Best practice: Build in a time frame that gives HR staff and employees the time they need. Benz recommended three weeks.

"People are always talking about learning from the best practices and success stories, but you can also learn a lot from other companies' mistakes," she noted. "When you prepare for enrollment in advance and anticipate issues—including those you and others have experienced in the past—you are better-equipped to avoid missteps. Your employees will notice and appreciate the extra effort."

Help Employees Ace Open Enrollment

"Open enrollment is often time-consuming and confusing for employees, but these choices can make a huge financial impact," said Julie Stich, CEBS, vice president of content at the International Foundation of Employee Benefit Plans, an association of benefit plan sponsors. She suggested that HR share the following advice with employees to help prepare them for the upcoming enrollment season:

- Take your time. Take time to really read through the enrollment materials you receive. If you are invited to a face-to-face meeting, make time to attend. It's possible you'll be offered different plan options and coverages this year. The better you understand the changes, the better decisions you'll make.

-

Take a trip down memory lane. Think back to what happened in your life this year. How often did you and your family members need medical services? What kind? Are any treatments ongoing? Think about any life changes that could affect the benefits you need, like a marriage or divorce, a child going off to college, or a spouse changing jobs.

- Look ahead. Consider what the next year will look like for you and your family. Are you planning to have a baby? Knee replacement surgery? A root canal? Does someone need braces? New glasses? Keep this in mind as you look at your coverage options.

- Dive into the details. It's important to note whether the plans' provider networks have changed. Make sure your doctors are still in-network. Is your chiropractor also covered? Does the plan cover orthodontics? Is your spouse's daily prescription drug covered, and did the coverage change? Also consider areas of need like access to specialists, mental health care, therapies, complementary and alternative medicine, and chronic care. Look at the options offered in all plans, including health, dental, vision and disability.

- Get out your calculator. Add up the amount you'll need to pay toward your health premium plus deductibles, co-payments (flat-dollar amounts) for prescriptions and doctor office visits, and co-insurance (a percentage of the cost you'll pay) for services. Understand what you'll be asked to pay if you seek care outside your network. This will give you a clearer picture of how much you're likely to spend. The plan that looks to be the cheapest option may not really be the cheapest for you.

- Determine what's right for you. Consider your comfort level with risk. If you want your family to be covered for every eventuality, a more traditional plan, if one is offered, might be right for you. If you're comfortable taking on some upfront costs, a high-deductible plan with a lower premium ight be your plan of choice.

- Take advantage of extras. Your employer may offer the option to reduce your health premiums in exchange for your participation in a wellness program or health-risk assessment. It may match some or all of the money you save in your 401(k) plan. It might let you set aside tax-deferred money into a health savings account or flexible spending account. Also, check with your employer to see if it offers voluntary insurance with a group discount and payroll deduction for premiums—like critical-illness, pet, auto and homeowners coverage. If these options work for your situation, sign up.

- Ask questions. Don't be shy about asking your HR or benefits department to explain something if you're not sure. They're there to help and want you to make the best decisions for your situation.

"Taking the time upfront to carefully choose the best options will help employees better manage their finances throughout the year, alleviating stress and promoting productivity," Stich said.

SOURCE: Miller, S. (24 September 2019) "Simple Open-Enrollment Tips That Can Make a Big Difference" (Web Blog Post). Retrieved from https://www.shrm.org/ResourcesAndTools/hr-topics/benefits/Pages/simple-open-enrollment-tips-make-a-big-difference.aspx

‘Eye’ spy a savings opportunity for health and vision benefits

The National Eye Institute reported that 61 million adults are at high risk for serious vision loss. Conventionally, vision benefits were offered as an elective, with coverage is focusing on vision tests or discounts for corrective eyewear. Read the following blog post to learn more about vision benefits.

Sixty-one million adults are at high risk for serious vision loss, according to the National Eye Institute, but most U.S. employers don’t include eye care as part of their benefits package. Vision benefits have traditionally been offered as an elective, where coverage is focused on vision tests or discounts for corrective eyewear.

This often results in inadequate coverage for employees and dependents, which can result in unrecognized and untreated issues that impact employee health and productivity, as well as an employer’s bottom line.

Comprehensive eye exams are recommended for adults under the age of 65 at least every two years, according to the American Optometric Association (AOA). These exams are the only way a doctor can detect signs and symptoms of serious conditions without cutting into or scanning body parts.

The total economic burden of eye disorders and vision loss in the U.S. was $139 billion in 2013, which includes $65 billion in direct medical costs strictly due to eye disorders and low vision. Loss of vision among workers results in $48 billion in lost productivity per year.

When it comes to benefit management priorities employers often focus more on chronic condition management. Yet, eye health is often linked to common chronic conditions including diabetes and hypertension. Without early detection of eye and vision health issues, employees cannot properly manage these conditions. Delaying medical treatment can lead to increased absenteeism and reduced productivity, eventually resulting in treatment that comes too late, and at a much higher price tag for employers, employees and family members.

About 68% of Americans with diabetes have been diagnosed with eye complications, many of which could have been prevented through a comprehensive eye exam. Diabetes is the leading cause of blindness among adults, according to the National Institutes of Health. Its prevalence is increasing as one in 10 people worldwide may be affected by 2040, according to research from the International Diabetes Federation.

Nearly half of Americans don’t know that diabetic eye diseases have visible symptoms, according to a 2018 AOA survey. More than one-third of respondents didn’t know a comprehensive eye exam is the only way to determine if a person’s diabetes will cause blindness. These exams, considered the gold standard in clinical vision care, should be covered under the employees’ medical benefits.

Three years ago the Midwest Business Group on Health began a collaboration with the AOA to better understand how employers think about and implement eye health and vision benefits. As part of this partnership, a no-cost eye care benefits toolkit was developed to support employers in evaluating their current eye health and vision care benefits to:

- Understand the importance of early detection so that employees can effectively manage chronic and more serious conditions

- Recognize how to integrate primary and preventive eye care into an overall medical benefit design

- Educate employees on the importance of periodic eye examinations

It’s important that employers better understand the impact of vision care benefits, including lower costs, better employee health, improved job satisfaction, better employee quality of life, and work productivity.

SOURCE: Larson, C. (20 September 2019) "‘Eye’ spy a savings opportunity for health and vision benefits" (Web Blog Post). Retrieved from https://www.benefitnews.com/opinion/vision-loss-resulting-in-billions-in-lost-productivity

DOL issues finalized overtime regulation

The DOL recently released their finalized overtime rule. This new rule raises the minimum salary level to $35,568 per year for a full-year worker to earn overtime wages. Read this blog post from Employee Benefit News to learn more about this new rule.

The DOL on Tuesday released its highly anticipated finalized overtime rule, raising the minimum salary level to $35,568 per year for a full-year worker to earn overtime wages.

“Today’s rule is a thoughtful product informed by public comment, listening sessions and long-standing calculations,” Wage and Hour Division Administrator Cheryl Stanton says in a statement. “The DOL’s wage and hour division now turns to help employers comply and ensure that workers will be receiving their overtime pay.”

The final rule, effective Jan. 1, 2020, updates the earnings thresholds necessary to exempt executive, administrative or professional employees from the FLSA’s minimum wage and overtime pay requirements, and allows employers to count a portion of certain bonuses (and commissions) toward meeting the salary level.

The new thresholds account for growth in employee earnings since the currently enforced thresholds were set in 2004. In the final rule, the department is:

- Raising the standard salary level from the currently enforced level of $455 to $684 per week (equivalent to $35,568 per year for a full-year worker);

- Raising the total annual compensation level for highly compensated employees from the currently-enforced level of $100,000 to $107,432 per year;

- Allowing employers to use nondiscretionary bonuses and incentive payments (including commissions) that are paid at least annually to satisfy up to 10% of the standard salary level, in recognition of evolving pay practices; and

- Revising the special salary levels for workers in U.S. territories and in the motion picture industry.

This finalized rule is a shift from the previous administration's proposed rule, which would have doubled the salary threshold.

Under the Obama administration, the Labor Department in 2016 raised the minimum salary to roughly $47,000, extending mandatory overtime pay to nearly 4 million U.S. employees. But the following year, a federal judge in Texas ruled that the ceiling was set so high that it could sweep in some management workers who are supposed to be exempt from overtime pay protections. Business groups and 21 Republican-led states then sued, challenging the rule.

The overturning of the 2016 rule that increased the salary level from the 2004 level has created a lot of uncertainty, says Susan Harthill, a partner with Morgan Lewis. The best way to create certainty is to issue a new regulation, which is what the administration's done, Harthill adds.

While the final rule largely tracks the draft, there are two changes that should be noted: the salary level is $5 higher and the highly compensated employee salary level is dramatically reduced from the proposed level, she says.

“This is an effort to find a middle ground, and while it may be challenged by either or maybe both sides, the DOL’s salary test sets a clear dividing line between employees who must be paid overtime if they work more than 40 hours per week and employees whose eligibility for overtime varies based on their job duties,” Harthill adds.

The DOL estimates 1.3 million employees could now be eligible for overtime pay under this rule (employees who earn between $23,600 and $35,368 no longer qualify for the exemption).

A majority of business groups were critical of Obama’s overtime rule, citing the burdens it placed particularly on small businesses that would be forced to roll out new systems for tracking hours, recordkeeping and reporting.

SHRM, for example, expressed it's opposition to the rule, noting it would have fundamentally changed the rules for employee classification, dramatically increased the salary under which employees are eligible for overtime and provided for automatic increases in the salary level without employer input.

“Today’s announcement finalizing DOL’s overtime rule provides much-needed clarity for workplaces," SHRM says in a statement. "This rule marks the first increase to the salary threshold since 2004 and gives employers more flexibility to plan for the future. We appreciate DOL’s willingness to work with SHRM, other organizations and America’s workers to enact an overtime rule that benefits both employers and their employees.”

But the finalized rule still will have implications for employers.

“Education and health services, wholesale and retail trade, and professional and business services, are the most impacted industries, according to DOL, but all industries are potentially impacted,” Harthill, also former DOL deputy solicitor of labor for national operations, adds. “Also often overlooked is the impact on nonprofits and state and local governments, which are subject to the FLSA and often have lower salaries.”

All companies should be taking a close look at their employees to make sure workers are properly classified, but what they do after that will depend entirely on individual business needs, she says. “Some will hire additional employees to reduce the amount of overtime, while others will just pay overtime if their workers in this salary bracket spend more than 40 hours a week on the job.”

Employers who haven’t already reviewed their exempt workforce should do so now, before the Jan. 1 effective date, Harthill advises.

“They can opt to pay overtime, raise salary levels above $35,368, or review and tighten policies to ensure employees do not work more than 40 hours per week,” she says. “There could be job positions that need to be reclassified and that might have a knock-on effect for employees who earn above the new salary level.”

Many employers increased their salaries when DOL issued the 2016 rule, and some states have higher salary levels, so not all businesses will need to make an adjustment. “But even those employers should review their highly compensated employees — they may still be exempt even if they earn less than $107,432 but the analysis will be more complicated,” she adds.

“We did not hear any objections from employers when these rules were initially proposed," adds Jason Hammersla, vice president of communications at the American Benefits Council. "That said, aside from the obvious compensation and payroll tax implications, this rulemaking is significant for employers who include overtime compensation in the formula for retirement plan contributions as it could increase any required employer contributions."

"The change could also affect plans that exclude overtime pay from the plan’s definition of compensation if the new overtime pay causes the plan to become discriminatory in favor of highly compensated employees," he adds.

SOURCE: Otto, N. (24 September 2019) "DOL issues finalized overtime regulation" (Web Blog Post). Retrieved from https://www.benefitnews.com/news/dol-issues-finalized-overtime-regulation

Health insurance surpass $20,000 per year, hitting a record

According to an annual survey of employers, the cost of family health coverage has now surpassed $20,000, a record high. The survey also revealed that while most employers pay most of the costs of coverage, workers' average contribution for a family plan is now $6,000. Read this blog post from Employee Benefit News to learn more.

The cost of family health coverage in the U.S. now tops $20,000, an annual survey of employers found, a record high that has pushed an increasing number of American workers into plans that cover less or cost more, or force them out of the insurance market entirely.

“It’s as much as buying a basic economy car,” said Drew Altman, chief executive officer of the Kaiser Family Foundation, “but buying it every year.” The nonprofit health research group conducts the yearly survey of coverage that people get through work, the main source of insurance in the U.S. for people under age 65.

While employers pay most of the costs of coverage, according to the survey, workers’ average contribution is now $6,000 for a family plan. That’s just their share of upfront premiums, and doesn’t include co-payments, deductibles and other forms of cost-sharing once they need care.

The seemingly inexorable rise of costs has led to deep frustration with U.S. healthcare, prompting questions about whether a system where coverage is tied to a job can survive. As premiums and deductibles have increased in the last two decades, the percentage of workers covered has slipped as employers dropped coverage and some workers chose not to enroll. Fewer Americans under 65 had employer coverage in 2017 than in 1999, according to a separate Kaiser Family Foundation analysis of federal data. That’s despite the fact that the U.S. economy employed 17 million more people in 2017 than in 1999.

“What we’ve been seeing is a slow, slow kind of drip-drip erosion in employer coverage,” Altman said.

Employees’ costs for healthcare are rising more quickly than wages or overall economy-wide prices, and the working poor have been particularly hard-hit. In firms where more than 35% of employees earn less than $25,000 a year, workers would have to contribute more than $7,000 for a family health plan. It’s an expense that Altman calls “just flat-out not affordable.” Only one-third of employees at such firms are on their employer’s health plans, compared with 63% at higher-wage firms, according to the Kaiser Family Foundation’s data.

The survey is based on responses from more than 2,000 randomly selected employers with at least three workers, including private firms and non-federal public employers.

Deductibles are rising even faster than premiums, meaning that patients are on the hook for more of their medical costs upfront. For a single person, the average deductible in 2019 was $1,396, up from $533 in 2009. A typical household with employer health coverage spends about $800 a year in out-of-pocket costs, not counting premiums, according to research from the Commonwealth Fund. At the high end of the range, those costs can top $5,000 a year.

While raising deductibles can moderate premiums, it also increases costs for people with an illness or who gets hurt. “Cost-sharing is a tax on the sick,” said Mark Fendrick, director of the Center for Value-Based Insurance Design at the University of Michigan.

Under the Affordable Care Act, insurance plans must cover certain preventive services such as immunizations and annual wellness visits without patient cost-sharing. But patients still have to pay out-of-pocket for other essential care, such as medication for chronic conditions like diabetes or high blood pressure, until they meet their deductibles.

Many Americans aren’t prepared for the risks that deductibles transfer to patients. Almost 40% of adults can’t pay an unexpected $400 expense without borrowing or selling an asset, according to a Federal Reserve survey from May.

That’s a problem, Fendrick said. “My patient should not have to have a bake sale to afford her insulin,” he said.

After years of pushing healthcare costs onto workers, some employers are pressing pause. Delta Air Lines Inc. recently froze employees’ contributions to premiums for two years, Chief Executive Officer Ed Bastian said in an interview at Bloomberg’s headquarters in New York last week.

“We said we’re not going to raise them. We're going to absorb the cost because we need to make certain people know that their benefits structure is real important,” Bastian said. He said the company’s healthcare costs are growing by double-digits. The Atlanta-based company has more than 80,000 employees around the globe.

Some large employers have reversed course on asking workers to take on more costs, according to a separate survey from the National Business Group on Health. In 2020, fewer companies will limit employees to so-called “consumer-directed health plans,” which pair high-deductible coverage with savings accounts for medical spending funded by workers and employers, according to the survey. That will be the only plan available at 25% of large employers in the survey, down from 39% in 2018.

Employers have to balance their desire to control costs with their need to attract and keep workers, said Kaiser’s Altman. That leaves them less inclined to make aggressive moves to tackle underlying medical costs, such as by cutting high-cost hospitals out of their networks. In recent years employers’ healthcare costs have remained steady as a share of their total compensation expenses.

“There’s a lot of gnashing of teeth,” Altman said, “but if you look at what they do, not what they say, it’s reasonably vanilla.”

SOURCE: Tozzi, J. (25 September 2019) "Health insurance surpass $20,000 per year, hitting a record" (Web Blog Post). Retrieved from https://www.benefitnews.com/articles/health-insurance-costs-surpass-20-000-per-year

6 voluntary benefits your employees want

Multigenerational workforces are no longer finding the run-of-the-mill benefits plans adequate. This is making voluntary benefits more important than ever in this age of the multigenerational workforce and a tight labor market. Read this blog post from for six voluntary benefits employees want.

In this age of the multigenerational workforce and a tight labor market, a one-size-fits-all group benefits model with medical, prescription, dental, vision and a retirement plan just doesn’t cut it. A workforce with Baby Boomers, Gen X’ers, Millennials and Generation Z means that employees are going to find the run-of-the-mill benefits plan inadequate. Ditto for job seekers.

What follows is that voluntary benefits are more important than ever. Offering a range of voluntary benefits can help meet the needs of employees at all life stages.

Voluntary benefits add value to benefit plans and are typically easy to administer. They’re low-to-no-cost because employees pay for them, and maintenance is often handled through a payroll deduction. Many voluntary benefits also offer guaranteed acceptance at a lower rate than medical benefits, so even if a small group within your company chooses a particular benefit, they’ll be covered.

This landscape is changing quickly. Here are six trending voluntary benefits your employees want.

Student loan debt repayment assistance

Debt among college graduates has grown to nearly $1.6 trillion. It’s preventing the largest employee segment at most companies from buying houses or cars, saving for retirement, having kids and getting married. To help employees repay their student loan debt, some employers are helping employees pay down student loan debt through a direct payroll deduction.

Others are offering a new, IRS-allowable retirement plan match swap where an employer can opt to increase its defined contribution match, enabling employees to reduce their retirement match and contribute funds to repaying student loans instead.

Interest in this benefit continues to grow. Employers looking to offer student loan debt repayment should be aware that not all platforms are created equal. Look out for high per-employee, per-month fees.

Individual long-term care

A growing number of people are beginning to understand the value of long-term care insurance because they have taken care of or currently care for a friend or relative who needs round-the-clock care. Long-term care insurance covers home or institutional care if a person is no longer able to perform at least two activities of daily living--eating, bathing, dressing, moving from a bed to a chair or using a toilet.

Employees are interested in buying long-term care insurance through their employer because they can offer better rates for simplified issue plans. If you plan to offer long-term care as an employer-sponsored benefit, I recommended rolling it out with a strategic project plan and a benefit counselor or a technology platform capable of providing decision-making tools for a smooth application process.

Executive reimbursement plans

Employee retention — especially executive retention — is on the minds of many employers in the midst of this thriving economy. Filling gaps in medical and prescription coverage is one way to provide executive teams with premium benefits they may be looking for.

Executive reimbursement plans provide reimbursement for out-of-pocket expenses, access to facilities and level of service not normally covered under most group health plans. Rather than simply increasing compensation to help cover out-of-pocket expenses, premiums for these plans are tax-deductible for the employer, and benefits are non-taxable for employees.

Executive individual disability insurance

Traditional employer-sponsored long-term disability (LTD) is likely not enough coverage for highly-compensated employees or some sales staff who depends heavily on commission and bonuses. Normally, LTD pays employees 50-70% of their salary up to a certain amount.

Employers can carve out additional coverage for employees based on their management level, performance or tenure. Individual disability insurance plans can protect employees until they turn 65; they can also protect job titles or levels until employees are well enough to return to work. Executive individual disability insurance, like executive reimbursement, can be offered as a form of compensation, or a form of financial asset protection for higher incomes.

Telemedicine

The rise of consumer-driven health plans has led to the need for telemedicine. Telemedicine provides a way for employees to see a physician or provider by video and get a diagnosis and/or prescription quickly. The success of telemedicine is leading some carriers to integrate it within their plan. However, standalones still exist and can provide employees with an easy way to get care faster and cheaper than before.

Pet Insurance

Pet parents spend nearly $70 billion on veterinarian costs for their pets, but just 10% of dogs and 5% of cats are covered by medical insurance. As pets begin to play a larger role in our lives, more employers are offering pet insurance to their employees to help defray the cost of unexpected medical expenses.

There are a number of plan options, and setting up a plan for employees’ pets is simple. However, it’s vital that employers do their research to ensure the veterinarian network includes the best vets.

As part of a voluntary benefit offering, be sure to develop a rollout strategy and communications plan so employees are thoroughly educated and you meet group minimums.

SOURCE: Park, N. (25 September 2019) "6 voluntary benefits your employees want" (Web Blog Post). Retrieved from https://www.benefitnews.com/list/6-voluntary-benefits-your-employees-want

Key elements to consider when researching financial wellness programs

With financial wellness programs becoming a staple employee benefit, organizations find themselves implementing programs that only offer a few tools or resources. Read the following blog post from Employee Benefit Advisor for key elements to consider when researching financial wellness programs.

Financial wellness programs are becoming a staple in the employee benefit universe. But what should a successful financial wellness program encompass? As a rapidly growing industry, we often lack a consistent definition for financial wellness. This leads to organizations believing they have implemented a financial wellness program, when they may only be offering a few tools like education or counseling.

I define financial wellness as the process by which an individual can efficiently and accurately assess their financial posture, identify personal goals, and be motivated to gain the necessary knowledge and resources to create behavioral change. Behavioral change will result in improved emotional and mental well-being, along with short- and long-term financial stability.

As the administrator of your company’s benefits, you are responsible for bringing the best possible solution to your employees. That’s a tough ask, given the growing number of service providers. So, what is the most efficient and effective way to assess financial wellness services to determine which solution best fits your organizational needs? Ask yourself these questions:

Does the platform offer a personal assessment of each employee’s current financial situation and help them identify their financial goals? If the answer is yes: Does the assessment return quantifiable and qualifiable data unique to each individual employee?

Does the platform address 100% of your employee base, including the least sophisticated employees at various levels of employment? Much of your ROI from a financial wellness program does not come from your top performers. It comes from creating behavioral changes within your employees who need the most financial guidance.

Does the platform integrate the various components to provide a personalized roadmap for each employee? It should connect program elements like personal assessments, educational resources, tools, feedback and solutions to ensure the employee is presented with a cohesive, comprehensive plan to attack and improve their financial situation.

Does the platform offer solutions for short-term financial challenges like cash flow issues, as well as long-term financial challenges associated with saving and planning? A major return on your investment comes from reduced employee stress, which is substantially driven by short-term needs versus long-term objectives. The program must help employees deal with current financial challenges before they can focus on their longer-term vision.

About 78% of U.S. workers live paycheck to paycheck to make ends meet, according to data from CareerBuilder.com. The need for financial wellness is clear, but there are consistent pillars that must be addressed in any successful financial wellness program to affect change: spend, save, borrow and plan. When evaluating financial wellness programs, it’s important that these dots all connect if you are truly going to motivate behavioral change and recognize the ROI of a comprehensive financial wellness program.

SOURCE: Kilby, D. (13 September 2019) "Key elements to consider when researching financial wellness programs" (Web Blog Post). Retrieved from https://www.employeebenefitadviser.com/opinion/key-considerations-for-employee-financial-wellness-programs

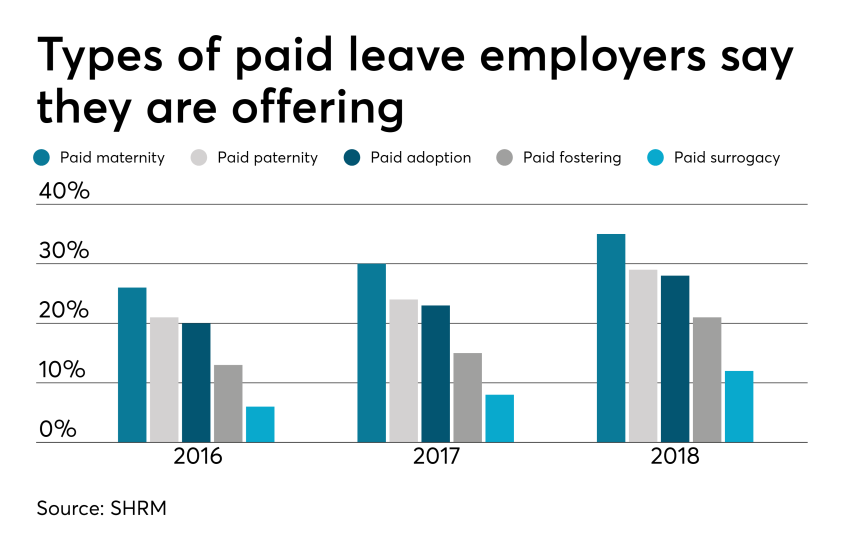

4 pitfalls of paid leave and how clients can avoid them

Employers are using paid leave options to help boost their employee benefits packages in efforts to better attract and retain talent. Read the following blog post from Employee Benefit Advisor for 4 common pitfalls of paid leave and how employers can avoid them.

Smart employers are boosting their benefits packages with paid family leave — the most coveted work perk among all generations. In today’s low unemployment environment, paid leave benefits can be a huge differentiator in attracting and retaining talent.

Smart employers are boosting their benefits packages with paid family leave — the most coveted work perk among all generations. In today’s low unemployment environment, paid leave benefits can be a huge differentiator in attracting and retaining talent.

But some employers are getting themselves into trouble in the process, facing accusations of gender discrimination or improper use of leave.

Here are four potential pitfalls of paid leave, and how employers can avoid them.

1. Be careful what you call “maternity leave.”

Employers have long been granting leave for new moms in the form of disability coverage. In fact, the top cause of short term disability is pregnancy. Disability insurance usually grants new moms six to eight weeks of paid leave to recover from childbirth.

Because this coverage applies to the medical condition of recovering from childbirth, it shouldn’t be lumped in with bonding leave.

Guidance from the Equal Employment Opportunity Commission says leave granted for new moms for bonding must also be extended to new dads, so separating disability leave from bonding leave is crucial to avoiding gender discrimination.

2. Don’t make gender assumptions.

The amount of bonding time for new parents after birth, adoption or fostering must be granted equally for men and women. Companies that don’t provide the same amount of paid leave for men and women may find themselves in a discrimination lawsuit.

It’s not just the time away from work that matters, but also the return-to-work support provided. If new moms are granted temporary or modified work schedules to ease the transition back to work, new dads must also have access to this.

Some companies may choose to differentiate the amount of leave and return-to-work support for primary or secondary caregivers. That’s compliant as long as assumptions aren’t made on which gender is the primary or secondary caregiver.

The best way to avoid potential gender discrimination pitfalls is to keep all parental bonding and related return-to-work policies gender neutral.

3. Avoid assuming the length of disability.

Be careful about assuming the length of time a new mom is disabled, or recovering medically, after birth. Typical coverage policies allot six to eight weeks of recovery for a normal pregnancy, so assuming a new mom may be out for 10 weeks might be overestimating the medical recovery time, and under-representing the bonding time, which must be gender neutral.

4. Keep up with federal, state and local laws.

Mandated leave laws are ever-evolving, so employers should consistently cross-check their policies with state and local laws. For instance, do local paid leave laws treat adoption the same as birth? Are multistate employers compliant? What if an employee lives in one state but works in another: Which state’s leave policies take precedence?

Partnering with a paid leave service provider can mitigate the risk of improperly administering leave. Paid leave experts can help answer questions, review guidelines and provide information regarding job-protecting medical or family leave.

They can also help flag potential pitfalls, ensuring leave requests from all areas of your company are managed uniformly and in accordance with state and federal laws, including the EEOC.

SOURCE: Bennett, A. (12 September 2019) "4 pitfalls of paid leave and how clients can avoid them" (Web Blog Post). Retrieved from https://www.employeebenefitadviser.com/list/4-pitfalls-of-paid-leave-and-how-clients-can-avoid-them

What would change if your employees were CEO for a day?

How is your workplace culture? New data shows that employees are 4.6 times more likely to contribute their best work when they feel like their voices are being heard. Read this blog post from Employee Benefits News to learn more about building a strong workplace culture.

When employees feel like their voices are being heard, they are reportedly 4.6 times more likely to contribute their best work, according to SalesForce data. Ultimately, knowing that the company is interested in what employees have to say builds trust and encourages loyalty among members of the workforce.

Respect is the most important leadership behavior, according to a Georgetown University survey of nearly 20,000 employees. More than merely listening, making employees a part of a two-way conversation shows that the company values their opinions.

With this in mind, we set out to develop a process to help Nearmap increase workplace communication. Along the way, we found that creating opportunities for interaction, encouraging honest participation and involving executive participation were all keys to building a stronger corporate culture.

Invite employee interaction

We recognized that we needed a conversation starter to open the lines of communication and spark a little enthusiasm. We discovered that engagement surveys work the best for our circumstances because they’re quick and easy to take, which results in high completion rates.

We like to include thought-provoking questions like “if you were CEO for a day, what is the one thing you would change?” to keep the employees engaged. At first, that particular question provided some of our most entertaining suggestions, including “free umbrellas for all,” “I would like the CEO’s paycheck,” “change my LinkedIn profile,” and “put margarita slushy machines in the kitchen.” When employees saw that the CEO responded to every answer, they realized that we were taking the feedback seriously, and that changed the tone of their responses.

Anonymity invites honest responses

It was essential to Nearmap that we collect unfiltered, honest feedback from our employees. This meant reassuring participants that their responses were completely anonymous. We believe this confidentiality encouraged authentic and candid submissions from employees that otherwise would have remained silent for fear of reprimand or judgment.

For instance, we’ve received excellent insights about driving the strategy and growth of the business, giving Nearmap valuable concepts that we’ve been able to embed into the business.

In addition, we present the survey results back to the employees so they can see how their thoughts align with those of their co-workers. We believe this commitment to being open is an excellent way to motivate honest dialog.

Executive participation leads by example

When the survey concludes, we group all of the responses under different headings, such as collaboration and communication, marketing, mission, planning, product, compensation, recognition, and general. Then, our CEO, Rob Newman, gets together with other executives to provide answers and comments on many of the submissions. In turn, those responses are shared with the employees via the HR newsletter and on our company collaboration app.

In reply to an inquiry about creating a green initiative for the company, our CEO shared a list of active programs that Nearmap was involved in to reduce not only our carbon footprint but also that of our customers as well.

While we may not know what we would change if we were the CEO for a day, we are convinced that employee interaction, honest responses and executive participation are reliable and important ways to make impactful connections with our employees and build a stronger corporate culture in our company.

SOURCE: Steel, S. (13 September 2019) "What would change if your employees were CEO for a day?" (Web Blog Post). Retrieved from https://www.benefitnews.com/opinion/what-would-change-if-your-employees-were-ceo-for-a-day

8 renewal considerations for 2020

Are you prepared for open enrollment 2020? With renewal season quickly approaching, plan administrators have a lot of considerations to make regarding employee health plans. Read the following blog post from Employee Benefit News for eight things to consider this year.

The triumphant return of the Affordable Care Act premium tax (the health insurer provider fee).

This tax of about 4% is under Congressional moratorium for 2019 and returns for 2020. Thus, fully insured January 2020 medical, dental and vision renewals will be about 4% higher than they would have been otherwise. Of note, this tax does not apply to most self-funded contracts, including so-called level-funded arrangements. Thus, if your plans are presently fully insured, now may be a good time to re-evaluate the pricing of self-funded plans.

Ensure your renewal timeline includes all vendor decision deadlines.

As the benefits landscape continues to shift and more companies are carving out certain plan components, including the pharmacy benefit manager, you may be surprised with how early these vendors need decisions in order to accommodate benefit changes and plan amendments. Check your contracts and ask your consultant. Further, it seems that our HRIS and benefit administration platforms are ironically asking for earlier and earlier decisions, even with the technology seemingly improving.

Amending your health plan for the new HSA-eligible expenses.

In July of this year, the U.S. Treasury loosened the definition of preventive care expenses for individuals with certain conditions.

While these regulations took effect immediately, they won’t impact your health plan until your health plan documents are amended. Has your insurer or third-party administrator automatically already made this amendment? Or, will it occur automatically with your renewal? Or is it optional? If your answer begins with “I would assume…,” double-check.

Amending your health plan for the new prescription drug coupon regulations.

As we discussed in July of this year, these regulations go into effect when plans renew in 2020. In short, plans can only prevent coupons from discounting plan accumulators (e.g., deductible, out-of-pocket maximum) if there is a “medically advisable” generic equivalent.

If your plan is fully insured, what action is your insurer taking? Does it seem compliant? If your plan is self-funded, what are your options? If you can keep the accumulator program and make it compliant, is there enough projected program savings to justify keeping this program?

Is your group life plan in compliance with the Section 79 nondiscrimination rules?

A benefit myth that floats around from time to time is that the first $50,000 in group term life insurance benefits is always non-taxable. But, that’s only true if the plan passes the Section 79 nondiscrimination rules. Generally, as long as there isn’t discrimination in eligibility terms and the benefit is either a flat benefit or a salary multiple (e.g., $100,000 flat, 1 x salary to $250,000), the plan passes testing. Ask your attorney, accountant, and benefits consultant about this testing. If you have two or more classes for life insurance, the benefit is probably discriminatory. If you fail the testing, it’s not the end of the world. It just means that you’ll likely need to tax your Section 79-defined “key employees” on the entire benefit, not just the amount in excess of $50,000.

Is your group life maximum benefit higher than the guaranteed issue amount?

Surprisingly, I still routinely see plans where the employer-paid benefit maximum exceeds the guaranteed issue amount. Thus, certain highly compensated employees must undergo and pass medical underwriting in order to secure the full employer-paid benefit. What often happens is that, as benefit managers turnover, this nuance is lost and new hires are not told they need to go through underwriting in order to secure the promised benefit. Thus, for example, an employee may think he or she has $650,000 in benefit, while he or she only contractually has $450,000. What this means is the employer is unknowingly self-funding the delta — in this example, $200,000. See the problem?

Please pick up your group life insurance certificate and confirm that the entire employer-paid benefit is guaranteed issue. If it is not, negotiate, change carriers, or lower the benefit.

Double-check that you haven’t unintentionally disqualified participant health savings accounts (HSAs).

As we discussed last December, unintentional disqualification is not difficult.

First, ensure that the deductibles are equal to or greater than the 2020 IRS HSA statutory minimums and the out-of-pocket maximums are equal to or less than the 2020 IRS HSA statutory maximums. Remember that the IRS HSA maximum out-of-pocket limits are not the same as the Affordable Care Act (ACA) out-of-pocket maximum limits. (Note to Congress – can we please align these limits?)

Also, remember that in order for a family deductible to have a compliantly embedded single deductible, the embedded single deductible must be equal to or greater than the statutory minimum family deductible.

Complicating matters, also ensure that no individual in the family plan can be subject to an out-of-pocket maximum greater than the ACA statutory individual out-of-pocket maximum.

Finally, did you generously introduce any new standalone benefits for 2020, like a telemedicine program, that Treasury would consider “other health coverage”? If yes, there’s still time to reverse course before 2020. Talk with your tax advisor, attorney, and benefits consultant.

Once all decisions are made, spend some time with your existing Wrap Document and Wrap Summary Plan Description.

For employers using these documents, it’s easy to forget to make annual amendments. And, it’s easy to forget, depending on the preparer, how much detail is often in these documents. For example, if your vision vendor changes or even if your vision vendor’s address changes, an amendment is likely in order. Ask your attorney, benefits consultant, and third party administrators for help.

SOURCE: Pace, Z. (Accessed 9 September 2019) "8 renewal considerations for 2020" (Web Blog Post). Retrieved from https://www.benefitnews.com/list/healthcare-renewal-considerations-for-2020

5 Questions Expecting Moms Have About Life Insurance

Are you considering life insurance? If this is your first time looking for coverage, you most likely have questions. Read this blog post from Life Happens for five questions expecting mothers typically ask when looking at life insurance.

If you are expecting a child and are considering life insurance, the first thing I have to say is—smart move! But if this is your first time looking for coverage, you may have questions. Here are some typical ones I’ve heard over the years:

1. What type of life insurance coverage is best for new parents—term or permanent?

Before figuring out what kind of coverage you need, you first have to understand how much death benefit you need to protect your family. You can do an easy calculation online to get a working idea of how much you may need with this Life Happens Life Insurance Needs Calculator.

Then you can move on to what kind of coverage—term or permanent—meets your needs. An advantage of term life insurance is that it costs less than permanent, at least initially. This makes it affordable for young families that may not have a lot of disposable income, but have a large need for coverage. Permanent insurance provides both lifelong coverage and a cash accumulation feature, which can be a valuable source of money that you can tap in the future.

Often, the best solution can be a combination of term and permanent life insurance. The term policy can give you extra coverage during the years when the children are at home, with the permanent policy offering lifelong coverage.

2. Should you consider different types of coverage if you are working mom versus a stay-at-home mom?

Both working and stay-at-home moms need protection because what they do for their families is so valuable. While a stay-at-home mom isn’t compensated for her work, if something were to happen to her, it would be expensive to replace all those things she does—from childcare to home care to ensuring the family gets where they need to go when they have to be there.

The difference between the two is that a working mother also contributes an income, which may be critical to the family financially. That means she needs to think about replacing that income when considering how much life insurance coverage she may need.

3. The company where I work offers life insurance, is that enough?

Group insurance is a great benefit to have, but it’s limited in a number of ways. First, the coverage is often a lump sum, such as $50,000, or it may be one to two times your salary. That may sound like a lot of money, but my question to you is: Honestly, how long would that money last? And what would happen to your family financially after that was gone?

Second, when you leave that job, you generally lose that coverage. If you don’t have an individual policy that you own, you’ll be leaving your family at risk. Think of how many times people change jobs, and you’ll quickly realize that group coverage, which is limited in scope and amount, is not a proper life insurance plan.

4. Are there any restrictions I have to consider now that I’m pregnant?

If it’s early in your pregnancy, and there are no medical complications, you should be able to get life insurance. If you’re farther along and there are medical issues, it may difficult to obtain. The life insurance company may want to wait until after your child is born. That’s why I advise those that are planning to have children to get the coverage as soon as possible.

5. What can I expect to pay for life insurance?

How much you pay for life insurance is based on a number of things but most importantly age and health. So, it depends on how old and how healthy you are! But here’s an example: A healthy 30-year-old woman could get $250,000 in life insurance coverage (for a 20-year level term policy for a nonsmoker) for about $13 a month. That’s certainly a lot of peace of mind for $13.

And don’t forget about your spouse or partner. The two of you could get $500,000 of combined coverage (using the example of two 30-year-olds that each get a $250,000 20-year level term policy) for right around $26 a month.

And my last piece of advice: talking with a life insurance agent at this stage can be very valuable. They can do a needs assessment and come up with the right type and amount of life insurance that works for your family budget. And what many people don’t realize is that an agent will sit down and offer this advice free of charge, with no strings attached. If you’d like help finding a life insurance professional, you can start here.

SOURCE: Feldman, M. (23 August 2019) "5 Questions Expecting Moms Have About Life Insurance" (Web Blog Post). Retrieved from https://lifehappens.org/blog/5-questions-expecting-moms-have-about-life-insurance/