Why a Strong Employee/Employer Relationship Is Important

Tied to the success of a company is the loyalty of its customers. While this customer-first mentality is necessary for the continuation of a company, employers sometimes forget to honor another intrinsic element of success and growth — the employee and employer relationship.

Employers are not drill sergeants who belt out orders for employees to follow. Why waste all that employee talent by burning them out? Work to build a strong and positive relationship with your employees, and they will grow as professionals and give back tenfold.

- Rethink Hierarchy: Help Employees Navigate the Organization

Employees have a place in the hierarchy of the company, but that doesn’t mean anyone should feel less than another or be demoralized. Every leader must understand the functions of their organization and its politics. Your organization’s culture sets the precedent for the professional personalities it hires. It should be clear to each employee why they were hired and why they are the best fit for a particular role.

Unfortunately, many employees simply exist in the vacuum of a cubicle and may not grow out of it. They feel boxed in and clueless about how to navigate the hierarchy and how to climb the ladder of success. An employee may need hand-holding or to be left alone, but that’s not the employee’s fault.

An employer has to find a way to meet them in the middle. Each employee has a hierarchy of needs that should be addressed, such as good benefits to meet basic needs, a positive work environment, a sense of place to develop a feeling of belonging and a way to become professionally self-actualized.

- Invest in Employee Networks and Loyalty

Just because you’ve moved up the ladder as a leader doesn’t mean you stop building relationships with those around you, including those under your supervision. You are a model of success for your employees, and you never know where your paths will lead or cross in the future.

Do your employees feel they can trust you? Do you empower and equip them with tools necessary to boost their influence and opportunities for success? Employee interoffice relationships and networks sculpt their reputation over the course of their careers.

Invest in employee networks to build loyalty and employee morale. Leaders should encourage networking inside and outside of the office. By strengthening influential networks, your employees will feel confident about their professional objectives and goals. They must learn that even professional relationships are not mutual all the time, and this negative exchange should be avoided. Loyalty is earned and learned when employees align with others who reciprocate support in networking, and that’s first gained from the employer.

Leaders should look at their own professional paths as an example for personal consideration. Name three others that have been in your network for years, and ask yourself if these are reciprocal relationships. Retrace the steps of your career, and remember leaders who held you back and why. Don’t be that leader. When employees climb the ladder, they will be in your network. Maintain reciprocal relationships with your employees, and teach them to do the same with others in their network.

- Broaden the Scope of Employee Experience

Don’t let employees become bored with their jobs. Of course, there are mundane tasks to every role that feel like chores, but employees should be allowed to challenge their knowledge. Let employees develop their skills by teaching them how to do the job of a leader. Broadening the scope of an employee’s experience prepares them for what comes next in their career, and they won’t fall short of expectations or feel their ambitions are neglected by an employer they trusted.

Many employers feel an employee should only understand what’s in their job description and nothing beyond fulfilling those duties. Wasn’t that why the employee was hired in the first place? An excellent leader sees the employee for their ambition and ability to grow, and then teaches them about the ecosystem of the workplace to advance.

Encourage employees to step up to the plate, beyond being a bench warmer, and take a swing at a big project or pitch an idea at a meeting. When an employee has the confidence to speak out and act independently, they gain the confidence to take risks, make involved decisions and lead.

Strong employee/employer relationships are vital to the success of the organization. The people and their relationships behind the scenes are the gears that move the mechanism of your company.

When your employees do their jobs well, achieve a new goal or do something successfully, reward them with networking opportunities and better benefits. Make the employee and employer relationship a strong and reciprocal one to be remembered for an entire career.

Read the original article.

Source:

Craig W. (20 September 2017). "Why a Strong Employee/Employer Relationship Is Important" [Web blog post]. Retrieved from address https://www.forbes.com/sites/williamcraig/2017/09/20/why-a-strong-employeeemployer-relationship-is-important/#480edb564d91

7 Ways Your Company Can Lead by Example by Supporting the Lives of Others

Be a business the gives back. In this article, adventure into some great ways to support your community and be a charitable employer.

Business moves the world. So how do you want your company to contribute?

To one degree or another, many of us feel the world today lacks quality leadership. But what better way to fight against that trend than by inspiring greatness in our future leaders? It all begins with leading by example. That’s a tall order, though, and not very specific — so let’s explore seven ways your company can assume thought leadership in the ongoing search for a better quality of life for all.

- Giving Back to the Community

If no person is an island unto themselves, that goes double for companies. We tend to think of our careers as somehow separate from the rest of waking life, but the truth is that communities and businesses are very much intertwined. Communities are responsible for the growth and success of businesses — and the other way around, too.

So? Give back as often as you can to the community that has made your business what it is today. We’ll talk in greater detail in a moment about what corporate citizenship should look like, but just getting that sentiment into your corporate culture and set of values is a great place to start.

- Be a Better Global Citizen

Making your business the source of positive influence in your community is one thing. But how are you being a global citizen?

Some folks in America seem to believe globalization should be feared and fought against, but rational business leaders know better. As the world draws closer together, we’ll be better prepared than ever to tackle some of the problems that affect us all in equal measure. But first we have to recognize our place in the larger global community.

One example would be The Exterior Company, based in Lancaster, PA, which recognizes their role on the global stage by contributing some of their profits to organizations committed to raising the standard of living in the poorer parts of the world.

- Know Your Values

Let’s get philosophical. Do you know what you value, personally? Would an onlooker identify your company as a “principled” one, even if they might not agree with the principles themselves?

The world needs businesses and leaders who know what they believe in. Not so we can blindly agree with them, but because all viewpoints help make the conversation a richer one. Even Hobby Lobby helped improve the conversation surrounding LGBTQ rights in America — even if they are, manifestly, and according to most Americans, standing on the wrong side of the issue.

American consumers wish for and respect companies that take the time to craft cohesive and forward-thinking sets of values. Why not show thought leadership here, and in the process, improve your company’s standing in the public eye?

- Donate Your Time

Money is a very valuable resource. But to many folks who don’t come from privilege, time is an even more precious commodity.

You can help support the lives of others — and lead by example in the process — by committing some of your free time to pro-social pursuits. Think of what would happen in the world if every employer allowed and encouraged their team members to commit some of their billable hours to charity work or another kind of community service.

Think of it like this: Corporate America boasts some of the most gifted and thoughtful people in the world. Folks for whom problem-solving comes naturally. What a shame and a waste it would be if all that talent were used merely to generate profits for private enjoyment.

- Raise the Standard of Living

If you’re new to business, you’ll recognize quickly that the conversation around workers’ well-being has changed in recent years. For example, global competition has thrown into sharp relief the ways that American corporate culture lags behind the rest of civilization. We have not yet joined the consensus on the fundamental right to paid sick leave and parental leave, for example.

There may be no better way to lead by example than to demonstrate how worthy your employees are of living high-quality lives. Your workers are your brand ambassadors — you want them to be able to go out into the world and proudly say their needs are taken care of. This improves the quality of our conversation everywhere.

-

- Raise Your Employees’ Awareness of the World Around Them

With FX Builds, we’ve helped establish a culture within our organization that ties daily excellence to funds-matching for charitable giving. We’ve already helped break ground on schools in distant countries where public education isn’t something that can be taken for granted.

The point, simply, as it is with other entries in this list, is to make your local team more aware of the larger world and to look for ways to live more fully and conscientiously within it. It’s probably easier than you might think. And if you do it thoughtfully, you can leverage the passion your team already brings to the table.

- Focusing on Sustainable Living

According to the scientific community, Earth is experiencing its sixth major extinction event even as we speak. Is that enough of a wake-up call?

It is clear that the individual has failed planet Earth. None of us could reuse enough plastic shopping bags in fifteen lifetimes to reverse the climate change that is already making life difficult in the poorer parts of our planet. And nothing about this is going to improve until we admit there’s a problem and agree on who’s in the best position to make a difference.

That means business leaders must actually lead by example, doing the heavy lifting the individual cannot on their own. It means taking advantage of cheaper-than-ever solar power everywhere you can afford to have it installed. It means not using more paper or other finite resources to do your work than is strictly necessary. It means turning off the computers in your office overnight.

To be perfectly honest, company leaders don’t have to look very far at all to lead the way in sustainable living. And if we can do it in the fight for sustainability, we can do it in every venue that requires decisive, progressive-minded leadership.

If every employer in the world used their resources and influence to help solve this and other crises we face in the world today, the future would be very bright indeed. Word is getting out that pro-social companies — being, after a fashion, like families themselves — are in a truly unique position to change life as we know it for the better.

Read the original article.

Source:

Craig W. (5 December 2017). "7 Ways Your Company Can Lead by Example by Supporting the Lives of Others" [Web blog post]. Retrieved from address https://www.forbes.com/sites/williamcraig/2017/12/05/7-ways-your-company-can-lead-by-example-by-supporting-the-lives-of-others/#786463064bbe

Building A Diverse Workforce In A Small Business

Shutterstock

There can be little argument against the value a diverse workplace. It’s a critical element of driving innovation, increasing creativity and securing market share, but diversity also makes growth and recruitment more manageable and helps to limit the word all employers want to avoid -- turnover. Diversity is significant enough that two-thirds of people polled in a Glassdoor survey said the level of diversity was important when evaluating job offers. This can prove to be a difficult task for a small business in the tech industry.

So what is workforce diversity? It’s more than simply not discriminating based on race, gender, national origin or disability. Diversity offers an alternative view or difference in opinions. Hiring employees with differing backgrounds in religion, from varying age ranges, sexual orientation, political affiliation, personality and education can become invaluable to an organization.

That being said, it can be nearly impossible to implement or force onto a set of employees. According to Harvard Business Review, researchers examined the success of mandated diversity training programs. While it’s simple enough to teach employees the right answers to questionnaires on bias or and appropriate responses for a given situation, the actual training rarely ever sticks, not more than a few days anyway. There have even been findings that suggest these mandated diversity training courses actually have adverse effects.

In the same article from HBR, managers said that when diversity training was mandatory, it is often met with confrontation and even anger. Some, in fact, reported an increase in animosity toward a minority group. On the other hand, when workers see the training as voluntary, the result is improved attitudes and an increase of 9-13% in the hiring of minorities five years from the training.

So if diversity is crucial to the success of a company or organization, but it's also something that can tough to implement, how does an employer ensure that they are fostering a work environment that is diverse? There are a few things employers can consider when they want to step up their game in building a more well-rounded and diverse workforce.

Evaluate The Hiring Process

Assess the level of diversity in the company. Does it reflect the general workforce of the industry or of the community? Figure out which departments are behind or lacking and what the source might be. Is a team diverse in most areas but still behind in management positions? Are managers hiring based on personal biases?

Top leadership needs to be an advocate for diversity in all hiring decisions, from the entry level to leadership positions. If there is a hiring test, see that managers are adhering to it. The HBR articles noted that even when hiring tests were in place, they were used selectively and that the results were ignored.

Having a hiring panel, or a system of checks and balances, would ensure that no one person would abuse the hiring process to lean too much on their own biases. Employers should also seek out new methods or places to network.

Mentoring Programs

Implementing a mentorship or sponsorship program will create a casual relationship between employees that will help alleviate some biases a manager might have and vice versa. Providing an opportunity for stewardship and responsibility allows the mentor to bestow knowledge on their mentee as they watch them grow.

Mentees will see the value in this experience and come to respect their mentor, laying away any preconceived biases or prejudices. They will become more invested in their work and the organization. Much like training programs, mentoring programs should be optional, not mandatory.

Inclusion

Similar to soldiers who serve together on the frontlines, employees who are part of a self-managed team and working as equals who work to complete projects will learn to dismiss biases on their own. Fostering an environment where employees can connect and collaborate increases engagement and allows for more contact than they may make when left to themselves.

In order to succeed in a global market, a tech organization must move past using "diversity" as a meaningless buzzword and step into action by developing and implementing an equal opportunity employment policy, following the Federal EEOC guidelines. Building and maintaining a diverse workforce is essential to growth and innovation in any industry, especially tech. But when handled poorly, or forced upon employees, it will cause more than a few headaches or even lawsuits. It requires change, a new take on leadership and creating a company culture based the business or service rather than a culture based on individual preferences or ideas.

Read the original article.

Source:

Cruikshank G. (4 December 2017). "Building A Diverse Workforce In A Small Business" [Web blog post]. Retrieved from address https://www.forbes.com/sites/forbestechcouncil/2017/12/04/building-a-diverse-workforce-in-a-small-business/#2b42986a4250

SaveSave

Employers using fast-feedback apps to measure worker satisfaction, engagement

In this article from Employee Benefit Advisors, we take a look at measuring worker satisfaction and engagement through the use of feedback applications. Let us know what your verdict is!

The days of employers conducting employee engagement surveys once every year might be coming to an end.

Thanks to “fast feedback” applications, employers can conduct quick online surveys of their employees to measure how engaged they are at their jobs. The data from these polls is then collated and presented, often in real time on dashboards, to employers to show their workforce’s level of engagement and satisfaction. Some of these web-based programs also can present CEOs with steps they can take to improve their environment and culture.

These tools are available from Culture Amp, Glint, TINYpulse, PeakOn and others.

One of the main benefits of fast feedback, according to Glint CEO Jim Barnett, is that it cuts down on “regrettable attrition,” which occurs when talented employees leave for better jobs.

Glint customers include eBay, Glassdoor, Intuit, LinkedIn and Sky Broadcasting. These clients send out e-mail invitations to workers and ask them to take a voluntary survey, which can feature either stock employee engagement questions or queries that can be fine-tuned for a specific workplace.

Glint recommends 10 to 20 questions per Pulse — what it calls employee engagement survey sessions — and results are sent back to the employer’s HR directors and senior executives. According to Barnett, the Pulses are confidential but not anonymous. Barnett explains that while anonymous surveys do not record the respondent’s name and job title, a confidential survey means that only Glint knows who took the Pulse. The employer is only presented data from specific job groups or job descriptors within an enterprise, such as a production team or IT support.

This month, Glint announced two new capabilities to its real-time employee feedback program, called Always-On and On-Demand Surveys. Always-On allows workers to express their concerns at any time and On-Demand Surveys gives managers and executives the opportunity to perform quick, ad hoc surveys of staffers.

“Some of our companies use the Always-On Survey if they want people on their team to give feedback at any time on a particular topic,” he says.

Firms also use fast feedback for onboarding new hires, Barnett says. Companies have set up Glint’s program to gauge new workers at their 30 and 60 day-mark of their employment to “see how that onboarding experience impacted their engagement,” he says.

Culture Amp also provides fast feedback tools via a library of survey templates that cover a range of employee feedback topics including diversity and inclusion, manager effectiveness, wellness and exit interviews. Culture Amp’s clients include Aligned Leisure, Box, Etsy, McDonalds, Adobe and Yelp.

“We encourage customers to customize surveys to make the language more relevant, and to ensure every question reflects something the company is willing to act on,” says Culture Amp CEO Didier Elzinga.

Culture Amp presents its survey results to employers via a dashboard that displays the top drivers of employee engagement in real time. “Users can then drill down to understand more about each question, including how participants responded across a range of different demographic factors,” Elzinga says.

Sometimes CEOs are presented with news they were not prepared to hear, according to Elzinga. Some customers take to the employee survey process with the mindset of ‘myth busting,’ he says. “They want to know if some truth they hold dear is actually just a story they’ve been telling themselves. Every now and then, an employee survey will provide surprising results to an HR or executive team,” he says. “Whether people go into a survey looking to bust myths or gather baseline data, the important part is being open to accepting the results.”

Glassdoor takes the pulse of its workforce

Glint customer Glassdoor, the online job recruitment site that also allows visitors to anonymously rate their current employer’s work environment, compensation and culture, not only urges its employees to rate the firm using its own tools, the company also uses Glint’s software to view employee engagement at a more granular level.

Glassdoor conducted its first Glint Pulse in October 2016 and has rolled out three since then. The next is scheduled for January 2018, according to Marca Clarke, director of learning and organizational development at Glassdoor.

“We looked at employee engagement and the things that drive discretionary effort [among employees who work harder],” Clarke says. “This is strongly correlated with retention as well.”

Clarke said that one Glint Pulse found that the employees’ view of Glassdoor culture varied from location to location. Of its 700-person workforce, people working in the newer satellite offices were happier than the employees in its Mill Valley, Calif., headquarters. She speculates that this response could be due to newer, more eager employees hired in brand new, recently opened offices.

“People think culture is monolithic that should be felt across the company but we could see that there was some variation from office to office. With Glint, we were able to slice the data not just by region and job function but [we could] go to the manager level to look at how people with different performance ratings think about the culture,” she says.

Recent research from Aon Hewitt found that a 5% increase in employee engagement is linked to a 3% lift in revenue a year later. According to Barnett, Glint clients that regularly conduct surveys and take steps to engage their employees often see a boost in the price of their company shares.

“Companies in the top quartile of Glint scores last year [saw] their stock outperform the other companies by 40%,” he says. “They now have the data and can see that employee engagement and the overall employee experience really do you have a dramatic impact on the result of their company.”

Read the original article.

Source:

Albinus P. (5 December 2017). "Employers using fast-feedback apps to measure worker satisfaction, engagement" [Web blog post]. Retrieved from address https://www.employeebenefitadviser.com/news/employers-using-fast-feedback-apps-to-measure-worker-satisfaction-engagement?brief=00000152-1443-d1cc-a5fa-7cfba3c60000

SaveSave

Benefits to plants at your desk

Leaves on trees have turned, and a walk to the office often feels like a walk through an icebox. Open windows are a thing of months past. Cooped up, breathing dry indoor air, no one could blame you for feeling down.

But you can brighten your mood and boost your health by adding a plant or two to your workspace. You don’t even need much natural light or a green thumb.

Plants bring a bit of nature inside, along with other good stuff.

They make people happy, and taking care of them can make people even happier. That’s especially true if you’re digging in a garden – horticultural therapy helps sharpen memory and cognitive skills – but desk-side pruning can do wonders for your mental state too.

Plants are also terrific air purifiers.

The air in your office (and home) might be more polluted than air outside – especially if you’re in a big city. Furniture, carpet, plastic items and other synthetic materials are to blame, according to the Environmental Protection Agency.

Plants help by wicking away airborne chemicals and the carbon dioxide we puff out, and then give us oxygen, research from NASA shows.

Four decades ago, NASA scientists found more than 100 volatile organic compounds floating through the air of the Skylab space station. The bad stuff came from synthetic materials off-gassing low levels of chemicals such as formaldehyde, benzene and trichloroethylene – known irritants and potential carcinogens that are in earthly buildings too.

When the chemicals are trapped in an area, people breathing within that same area can get sick because the air isn’t getting “the natural scrubbing by Earth’s complex ecosystem,” as NASA puts it.

Hail plants.

Here are two that demand next to nothing and tolerate very low light (but are just as happy with lots of it). Expect them to live for years and years, without repotting. I speak from experience, but you’ll also find them on plenty of lists and in lots of books about easy-care plants that are good for your health.

Snake Plant or Mother-In-Law’s Tongue (Sansevieria trifasciata)

A sturdy plant with upright and stiff leaves. Ideally, its soil should dry out between waterings. It will grow bigger and look better if you water it as soon as the soil dries (not wait forever) and if it’s in medium light. But it still will live for months if you ignore it, and spring back to robust happiness when you give it a little love.

Pothos (Epipremnum aureum)

A flowing plant with vine-like stems that can easily take over your desk. Ideally, its soil should stay a little moist. But if you let the soil dry out completely, you can jolt the plant back to life with watering. It’s perfectly happy with all kinds of lighting, including florescent, but it will be fuller with better color when it gets decent natural light.

Read the original article.

Source:

Malek M. (4 December 2017). "Benefits to plants at your desk" [web blog post]. Retrieved from address https://workwell.unum.com/2017/12/3255/

I Have Life Insurance Through My Employer. Why Do I Need Another Policy?

Life Happens in a Heartbeat - Stay Prepared With Saxon Life Insurance.

Although it is a subject no one wants to talk about, Life Insurance may be one of the best purchases you ever make.

Have you considered what would happen if you were not there to take care of your loved ones? Life insurance plans are about preparing for the unexpected. While nothing can replace you, having Life Insurance helps ensure that your family and loved ones would be financially stable if anything was to ever happen to you. Check out this article from Life Happens on the importance of obtaining Life Insurance - even if it's already offered through your employer.

One of the perks of having a full-time job with a good company is the benefits package that comes with it. Often, those benefits include life insurance coverage, which is great. And everyone who can get life insurance at work should definitely take it, as there are many advantages to company-funded life insurance, also known as group life insurance. These advantages include:

1. Easy qualification. Often, enrollment into group life insurance is automatic. That means everyone qualifies, as there is no medical exam required. So people who have preexisting health conditions, like diabetes or previous heart attack, can get life insurance at work, and may get a better rate compared with what an individual life insurance policy might cost them.

2. Lower costs. Employers’ insurance plans tend to be paid for or subsidized by the company, giving you life insurance at a low cost or even free. You may even have the option to buy additional coverage at low rates. Costs tend to be lower for many people because with group plans, the cost per individual goes down as the plan enlarges.

3. Convenience. It’s easy to subscribe to an employer’s life insurance plan without much effort on your part and if a payment is required, it’s easily deducted from your paycheck in much the same way as your medical costs are deducted.

These are all great advantages, but are these the only considerations that matter when it comes to life insurance? The answer, of course, is no.

Life insurance should first and foremost fit the purpose—it should meet your needs.

Life insurance should first and foremost fit the purpose—it should meet your needs. And the primary purpose of life insurance is to care for those left behind in the event of your death. With group life insurance, it’s often set at one or two times your annual salary, or a default amount such as $25,000 or $50,000. While this sounds like a lot of money, just think of how long that would last your loved ones. What would they do once that ran out?

There are several other disadvantages to relying on group insurance alone:

1. If your job situation changes, you’ll lose your coverage. Whether the change results from being laid off, moving from full-time to part-time status or leaving the job, in most cases, an employee can’t retain their policy when they leave their job.

2. Coverage may end when you retire or reach a specific age. Many people tend to lose their insurance coverage when they continue working past a specified age or when they retire. This means losing your insurance when you need it most.

3. Your employer can change or terminate the coverage. And that can be without your consent, since the contract is between your employer and the insurer.

4. Your options are limited. This type of coverage is not tailored to your specific needs. Furthermore, you may not be able to buy as much coverage as you need, leaving you exposed.

Importance of Buying a Separate Life Insurance Policy

It’s for these reasons you should get an individual life insurance policy that you personally own, in addition to any group life insurance you have. Individual life insurance plans offer superior benefits, and regardless of your employer or employment status, they remain in place and can be tailored to meet your needs and circumstances.

Most importantly, an individual life insurance policy will fit the purpose for which you purchase it—to ensure your dependents continue to have the financial means to keep their home and lifestyle in the unfortunate event that you’re no longer there to care for them.

Don't wait to protect your livelihood. Set up an appointment with one of our life insurance specialists here at Saxon by clicking this link.

Source:

Medina F. (19 June 2017). "I Have Life Insurance Through My Employer. Why Do I Need Another Policy?" [Web blog post]. Retrieved from address https://www.lifehappens.org/blog/i-have-life-insurance-through-my-employer-why-do-i-need-another-policy/

Do I Really Need Life Insurance?

At Saxon, we care greatly about others taking responsibility for their livelihood by applying for and obtaining life insurance. If you're not quite convinced you need to speak with one of our life insurance specialists, then take a glance at this article. Life insurance can help anyone - from single millennials to adults with mouths to feed. Don't let money or excuses keep you from protecting everything you've worked so hard for.

Let’s face it. Most people put off buying life insurance for any number of reasons—if they even understand it. Take a look at this list—do any of them sound like you?

1. It’s too expensive. In the ever-burgeoning budget of a young family, things like day care and car payments and possibly student loans eat up a good chunk of the money each month, and a lot of people think that life insurance is just outside those “necessities” when money’s tight. Life insurance is often not nearly as expensive as you might think, especially when you can get a good policy for less than the cost of a daily cup of coffee at the local café. If money’s tight now, what if something happens to you? Here’s more information about the true cost of life insurance.

2. That’s that stuff for babies and old people, right? People of a certain age remember Ed McMahon telling them their grandparents couldn’t be turned down for any reason and figure that’s the target demographic for life insurance. You might have been offered a small permanent insurance policy for your newborn, attractively presented with a cherubic infant on the envelope. The truth of the matter is that these are very specific insurance products—just as there are many insurance products for adults in their working years.

3. I’m strong and healthy! You eat right, you stay active, and everyone admires how grounded and centered you are. You passed your last physical with flying colors! That’s GREAT! But you’re neither immortal nor indestructible. It’s not even that something could happen to you—though it could—so much as when you’re at your strongest and healthiest, there’s no better time to get a policy to protect your loved ones. If you fall seriously ill or suffer significant injury later, it will make it tough to get that kind of policy, if any at all.

4. I have life insurance through my job. Many people are offered life insurance as part of their employee benefit coverage –and often, it’s the first time they encounter life insurance and have no idea that a $50,000 policy, or one or two times their salary, isn’t as much as they think it is. It sounds like a lot of money (and it is!), until you figure that it has to cover some or all the expenses for your loved ones in your absence. Plus, if you leave the job, it’s typically the type of insurance that doesn’t “move on” with you.

5. I don’t have kids. Sure, kids are a big reason why some people get life insurance, but that’s not the only reason for needing protection. If there is anyone in your life who would suffer financially from your loss—your spouse or live-in partner, a sibling, even your parents—a life insurance policy goes a long way in making sure everyone’s still OK even if something happens to you.

6. Life insurance—it’s on my list … eventually. There’s no deadline on life insurance, no mandate from the government on purchasing it. Your parents may have never talked to you about its importance, and it’s certainly not the most invigorating topic for conversation. But don’t let your “eventually” turn into your loved ones’ “if only.”

Don't wait to protect your livelihood. Have a chat with a specialist at Saxon Financial today by visiting this link.

Learn about the different types of life insurance here.

You can read the original article here.

Source:

Life Happens (n.d.). "Do I Really Need Life Insurance?" [Web blog post]. Retrieved from address https://www.lifehappens.org/insurance-overview/life-insurance/who-needs-life-insurance-reasons-dont-buy/

New Regulations Broadening Employer Exemptions to Contraceptive Coverage: Impact on Women

You can read the original article here.

Source:

Sobel L., Salganicoff A., Rosenzweig C. (6 October 2017). "New Regulations Broadening Employer Exemptions to Contraceptive Coverage: Impact on Women" [Web Blog Post]. Retrieved from address https://www.kff.org/womens-health-policy/issue-brief/new-regulations-broadening-employer-exemptions-to-contraceptive-coverage-impact-on-women/

The Trump Administration has issued new regulations that significantly broaden employers’ ability to be exempt from the Affordable Care Act’s (ACA) contraceptive coverage requirement. The regulation opens the door for any employer or college/ university with a student health plan with objections to contraceptive coverage based on religious beliefs to qualify for an exemption. Any nonprofit or closely-held for-profit employer with moral objections to contraceptive coverage also qualifies for an exemption. Their female employees, dependents and students will no longer be entitled to coverage for the full range of FDA approved contraceptives at no cost.

On October 6, 2017, the Trump Administration issued two new regulations greatly expanding the types of employers that may be exempt from the Affordable Care Act’s (ACA) contraceptive coverage requirement. These regulations are a significant departure from the Obama-era regulations that only granted an exception to houses of worship. One of the regulations allows nonprofits or for-profit employer with an objection to contraceptive coverage based on religious beliefs to qualify for an exemption and drop contraceptive coverage from their plans. The other regulation also exempts all but publicly traded employers with moral objections to contraception from rule. These new policies, effective immediately, also apply to private institutions of higher education that issue student health plans. The immediate impact of these regulations on the number of women who are eligible for contraceptive coverage is unknown, but the new regulations open the door for many more employers to withhold contraceptive coverage from their plans.

Contraceptive coverage under the ACA has made access to the full range of contraceptive methods affordable to millions of women. This provision is part of a set of key preventive services that has been identified by the Health Resources and Services Administration (HRSA) for women that must be covered without cost-sharing. Since it was first issued in 2012, the contraceptive coverage provision has been controversial. While very popular with the public, with over 77% of women and 64% of men reporting support for no-cost contraceptive coverage, it has been the focus of litigation brought by religious employers, with two cases (Zubik v Burwell and Burwell v Hobby Lobby) reaching the Supreme Court. This brief explains the contraceptive coverage rule under the ACA, the impact it has had on coverage, and how the new regulations issued by the Trump Administration change the contraceptive coverage requirement for employers and affect women’s coverage.

How do the new regulations change contraceptive coverage requirements for employers?

Since they were announced in 2011, the contraceptive coverage rules have evolved through litigation and new regulations. Most employers were required to include the coverage in their plans. Houses of worship could choose to be exempt from the requirement if they had religious objections. This exception meant that women workers and female dependents of exempt employers did not have guaranteed coverage for either some or all FDA approved contraceptive methods if their employer had an objection. Religiously affiliated nonprofits and closely held for-profit corporations were not eligible for an exemption, but could choose an accommodation. This option was offered to religiously affiliated nonprofit employers and then extended to closely held for-profitsafter the Supreme Court ruling in Burwell v. Hobby Lobby. The accommodation allowed these employers to opt out of providing and paying for contraceptive coverage in their plans by either notifying their insurer, third party administrator, or the federal government of their objection. The insurers were then responsible for covering the costs of contraception, which assured that their workers and dependents had contraceptive coverage while relieving the employers of the requirement to pay for it.

As of 2015, 10% of nonprofits with 5,000 or more employees had elected for an accommodation without challenging the requirement. This approach, however, has not been acceptable to all nonprofits with religious objections.1 In May 2016, the Supreme Court remanded Zubik v. Burwell, sending seven cases brought by religious nonprofits objecting to the contraceptive coverage accommodation back to the respective district Courts of Appeal. The Supreme Court instructed the parties to work together to “arrive at an approach going forward that accommodates petitioners’ religious exercise while at the same time ensuring that women covered by petitioners’ health plans receive full and equal health coverage, including contraceptive coverage.”2

On October 6, 2017, the Trump Administration issued new regulations greatly expanding eligibility for the exemption to all nonprofit and closely-held for-profit employers with objections to contraceptive coverage based on religious beliefs or moral convictions, including private institutions of higher education that issue student health plans (Figure 1). In addition, publicly traded for-profit companies with objections based on religious beliefs also qualify for an exemption. There is no guaranteed right of contraceptive coverage for their female employees and dependents or students. Table 1 presents the changes to the contraceptive coverage rule from the Obama Administration in the new Interim Final regulations issued by the Trump Administration.

Figure 1: Employers Objecting to Contraceptive Coverage: Exemptions and Accommodations Under the Trump Administration Regulations

The accommodation will be available to employers that previously qualified for the accommodation. They now will also have the choice of an exemption. The federal departments issuing the regulations posit that these new rules will have limited impact on the number of women losing contraceptive coverage. However, it is not clear how many employers previously utilizing the accommodation will now opt for an exemption, resulting in the loss of contraceptive coverage for their employees and dependents. In addition, there are also an unknown number of organizations that were not previously eligible for either the accommodation or exemption that may now opt for an exemption. These new regulations create two new categories of employers who can now qualify for an exemption or can voluntarily chooses an accommodation: 1) publicly traded for-profit companies with a religious objection and 2) nonprofit and closely held for-profit employers who have a moral objection to contraceptives, a considerably larger pool of employers than when the exemption was available only to those who were employees of a house of worship or who were eligible for an accommodation in the past.

| Table 1: Summary of Changes in the Contraceptive Coverage Regulations for Objecting Entities | ||

| Obama Administration August 2012 to October 5, 2017 |

Trump Administration Effective October 6, 2017 |

|

| What types of contraceptives must plans cover without cost-sharing? | At least one of each of the 18 FDA approved contraceptive methods for women, as prescribed, along with counseling and related services must be covered without cost-sharing. | No change |

| Are any employers “exempt” from the contraceptive mandate? |

|

|

| Who pays for contraceptive coverage for employees of organizations receiving an exemption? |

|

No change |

What type of employers may seek an “accommodation” to avoid paying for contraceptives in their plans? |

|

|

| Who pays for contraceptive coverage for employees of organizations receiving an accommodation? |

|

No change |

| When can entities change from an accommodation to an exemption? | N/A |

|

How has the contraceptive coverage rule affected women?

Contraceptive use among women is widespread, with over 99% of sexually-active women using at least one method at some point during their lifetime.3 Contraceptives make up an estimated 30-44% of out-of-pocket health care spending for women.4 Since the implementation of the ACA, out-of-pocket spending on prescription drugs has decreased dramatically (Figure 2). The majority of this decline (63%) can be attributed to the drop in out-of-pocket expenses on the oral contraceptive pill for women.5 One study estimates that roughly $1.4 billion dollars per year in out-of-pocket savings on the pill resulted from the ACA’s contraceptive mandate.6 By 2013, most women had no out-of-pocket costs for their contraception, as median expenses for most contraceptive methods, including the IUD and the pill, dropped to zero.7

Figure 2: The Contraceptive Coverage Policy Has Had a Large Impact on Out-Of-Pocket Spending in a Short Amount of Time

This provision has also influenced the decisions women make in their choice of method. After implementation of the ACA contraceptive coverage requirement, women were more likely to choose any method of prescription contraceptive, with a shift towards more effective long-term methods.8 High upfront costs of long-acting methods, such as the IUD and implant, had been a barrier to women who might otherwise prefer these more effective methods. When faced with no cost-sharing, women choose these methods more often9, with significant implications for the rate of unintended pregnancy and associated costs of childbirth.10

Finally, decreases in cost-sharing were associated with better adherence and more consistent use of the pill. This was especially true among users of generic pills. One study showed that even copayments as low as $6 were associated with higher levels of discontinuation and non-adherence,11 increasing the risk of unintended pregnancy.

Do states with no-cost contraceptive coverage laws allow exemptions to objecting entities?

The federal standards under Affordable Care Act created a minimum set of preventive benefits that applied to most health plans regulated by the federal government (self-funded plans, federal employee plans) and states (individual, small and large group plans), including contraceptive coverage for women with no cost-sharing. States have also historically regulated insurance, and many have had mandated minimum benefits for decades. State laws, however, have more limited reach in that they only apply to state regulated fully insured plans, do not have jurisdiction over self-funded plans, where 61% of covered workers are insured.12 In self-funded plans, the employer assumes the risk of providing covered services and usually contracts with a third party administrator (TPA) to manage the claims payment process. These plans are overseen by the Federal Department of Labor under the Employer Retirement Income Security Act (ERISA) and are only subject to federally established regulations.13 The ACA sets a minimum standard of coverage for preventive services for all plans. However, state laws regulating insurance, including contraceptive coverage, can require fully insured plans to provide coverage beyond the federal standards.

Eight states have strengthened and expanded the federal contraceptive coverage requirement (CA, IL, MD, ME, NV, NY, OR, VT). Another 20 states have contraceptive equity laws that require plans to cover contraceptives if they also provide coverage for prescription drugs but they do not necessarily require coverage of all FDA-approved contraceptives or ban cost-sharing (Figure 3).

Figure 3: Many States Have Contraceptive Coverage Requirements

Many of the 28 states that have passed contraceptive coverage laws (both equity and no-cost coverage) have a provision for exemptions, but the laws vary from state to state and only apply to fully insured plans. This means that there may be a conflict between the state and federal requirements when it comes to religious exemptions. In some states with a contraceptive coverage requirement, some employers who are eligible for an exemption under federal law will not qualify for an exemption under state law (Table 2). Employers in those states will have to have to meet the standards established by their state even though they may qualify for an exemption based on the new federal regulations. This conflict may set the stage for future litigation.

| Table 2: State Requirements for No-Cost Contraceptive Coverage | |||||||

| StateDate Effective | Applies to | Coverage required without cost sharing | Exemptions allowed | ||||

| Private plans | Medicaid | With RX all FDA approved | OTC | Vasectomy | Religious | Moral | |

| CaliforniaJanuary 2015 | X | MCOs | X | Narrowly defined nonprofit religious employers | None | ||

| IllinoisJanuary 2017 | X | X | X except male condoms |

Any employer, or insurer with a religious objection | Any employer, or insurer with a moral objection | ||

| MarylandJanuary 2018 | X | X | X | X | X | Religious organizations if the coverage conflicts with the organization’s bona fide religious beliefs and practices | None |

| MaineJanuary 2019 | X | X | Narrowly defined nonprofit religious employers | None | |||

| NevadaJanuary 2018 | X | X | X | Insurers affiliated with a religious organization | None | ||

| New YorkAugust 2017 | X | X | Narrowly defined nonprofit religious employers* | None | |||

| OregonAugust 2017 | X | X | X | Narrowly defined nonprofit religious employers | None | ||

| VermontOctober 2016 | X | X – and all other public health assistance programs | X | X | None | None | |

| NOTES: *Requires the insurer to offer a rider to policyholders so that women will have contraceptive coverage. SOURCE: Kaiser Family Foundation analysis of state laws and regulations. |

|||||||

Conclusion

The Trump Administration’s new regulations substantially expand the exemption to nonprofit and for-profit employers, as well as to private colleges or universities with religious or moral objections to contraceptive coverage. It is unknown how many of these employers and colleges will maintain coverage through the accommodation as before and how many will now opt for the exemption leaving their students, employees and dependents without no-cost coverage for the full range of contraceptive methods. As a result of the new regulation, choices about coverage and cost-sharing will be made by employers and private colleges and universities that issue student plans. For many women, their employers will determine whether they have no-cost coverage to the full range of FDA approved methods. Their choice of contraceptive methods may again be limited by cost, placing some of the most effective yet costly methods out of financial reach.

You can read the original article here.

Source:

Sobel L., Salganicoff A., Rosenzweig C. (6 October 2017). "New Regulations Broadening Employer Exemptions to Contraceptive Coverage: Impact on Women" [Web Blog Post]. Retrieved from address https://www.kff.org/womens-health-policy/issue-brief/new-regulations-broadening-employer-exemptions-to-contraceptive-coverage-impact-on-women/

What's the Dish? A Family Recipe for Salsa Lovers

In this month's Dish, we bring you the delicious "Dine In" and "Dine Out" choices from our very own, Abby Graham!

Abby Graham is a Wellness Director Saxon Financial Services. She has been in the insurance, health and wellness industry for over 12 years. Prior to joining Saxon Financial, she spent the last 7 years working for Humana/HumanaVitality. She is passionate about making sure members understand their medical and wellness benefits as well as how to maximize their potential.

Abby holds a degree in Human Resource Development from the University of Tennessee. She has also received her Group Benefits Disability Specialist (GBDS) certification.

She is an active member and board member of the Cincinnati Modern Quilt Guild. Abby also enjoys sewing, quilting, and spending time with her husband, Jon and her son, Carter.

Stay In:

Abby's favorite family recipe is Corn Avocado Salsa. She and her husband make it together. It’s best in the summer when the tomatoes are ripe and the corn is sweet!

1 ripe tomato

1 avocado

1 ear of corn

½ cup chopped cilantro

1 sweet onion

1 jalapeno

2-3 garlic cloves

1 ripe lime

Salt to taste

Grill the tomato until the skin is cracked and peeling off. Cut the avocado and grill it face down for about 5 minutes. Grill the corn until it is cooked all the way. In the meantime, finely chop the onion, jalapeno, cilantro and garlic cloves. Squeeze ½ of the lime over onion, jalapeno, cilantro and garlic combination.

Once tomato, avocado, and corn are finished grilling, cut corn off of the cob, and peel skin off of tomato. Dice tomato and avocado and add to chopped mix. Add salt to taste and serve warm with tortilla chips!

Dine Out:

Her favorite place to Dine Out is Dilly Café. Want driving directions? Get them here.

Our favorite restaurant is the Dilly Café in Mariemont. The outside seating is perfect on a nice night and/or when we have our little one with us. They generally have a band playing, the food is excellent, and the beer and wine list are great! Their crab cakes, wings and burgers are my favorites!

YUM! We hope you enjoy Abby's recipe and dining suggestions. We know we will!

The Medicare Part D Prescription Drug Benefit

Below we have an article from the Kaiser Family Foundation providing detailed information and graphics on the benefit of the Medicare Prescription Drug Plan.

You can read the original article here.

Medicare Part D is a voluntary outpatient prescription drug benefit for people on Medicare that went into effect in 2006. All 59 million people on Medicare, including those ages 65 and older and those under age 65 with permanent disabilities, have access to the Part D drug benefit through private plans approved by the federal government; in 2017, more than 42 million Medicare beneficiaries are enrolled in Medicare Part D plans. During the Medicare Part D open enrollment period, which runs from October 15 to December 7 each year, beneficiaries can choose to enroll in either stand-alone prescription drug plans (PDPs) to supplement traditional Medicare or Medicare Advantage prescription drug (MA-PD) plans (mainly HMOs and PPOs) that cover all Medicare benefits including drugs. Beneficiaries with low incomes and modest assets are eligible for assistance with Part D plan premiums and cost sharing. This fact sheet provides an overview of the Medicare Part D program and information about 2018 plan offerings, based on data from the Centers for Medicare & Medicaid Services (CMS) and other sources.

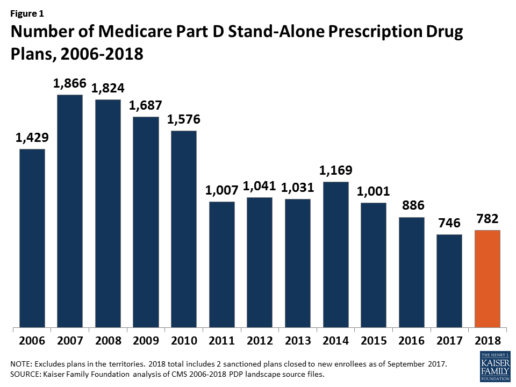

Medicare Prescription Drug Plan Availability in 2018

In 2018, 782 PDPs will be offered across the 34 PDP regions nationwide (excluding the territories). This represents an increase of 36 PDPs, or 5%, since 2017, but a reduction of 104 plans, or 12%, since 2016 (Figure 1).

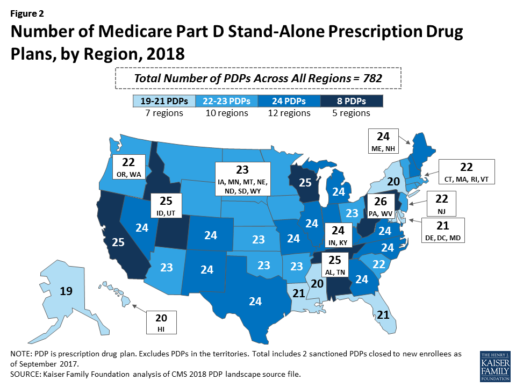

Beneficiaries in each state will continue to have a choice of multiple stand-alone PDPs in 2018, ranging from 19 PDPs in Alaska to 26 PDPs in Pennsylvania/West Virginia (in addition to multiple MA-PD plans offered at the local level) (Figure 2).

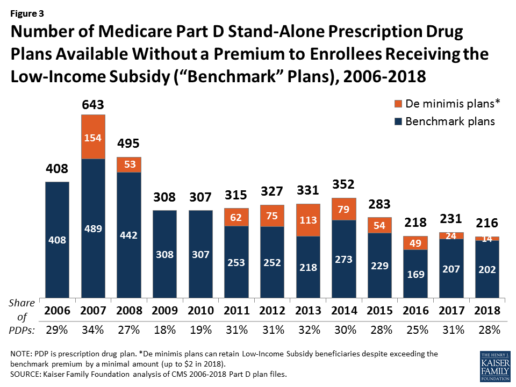

Low-Income Subsidy Plan Availability in 2018

Through the Part D Low-Income Subsidy (LIS) program, additional premium and cost-sharing assistance is available for Part D enrollees with low incomes (less than 150% of poverty, or $18,090 for individuals/$24,360 for married couples in 2017) and modest assets (less than $13,820 for individuals/$27,600 for couples in 2017).1

In 2018, 216 plans will be available for enrollment of LIS beneficiaries for no premium, a 6% decrease in premium-free (“benchmark”) plans from 2017 and the lowest number of benchmark plans available since the start of the Part D program in 2006. Roughly 3 in 10 PDPs in 2018 (28%) are benchmark plans (Figure 3).

Low-Income Subsidy Plan Availability in 2018

Through the Part D Low-Income Subsidy (LIS) program, additional premium and cost-sharing assistance is available for Part D enrollees with low incomes (less than 150% of poverty, or $18,090 for individuals/$24,360 for married couples in 2017) and modest assets (less than $13,820 for individuals/$27,600 for couples in 2017).1

In 2018, 216 plans will be available for enrollment of LIS beneficiaries for no premium, a 6% decrease in premium-free (“benchmark”) plans from 2017 and the lowest number of benchmark plans available since the start of the Part D program in 2006. Roughly 3 in 10 PDPs in 2018 (28%) are benchmark plans (Figure 3).

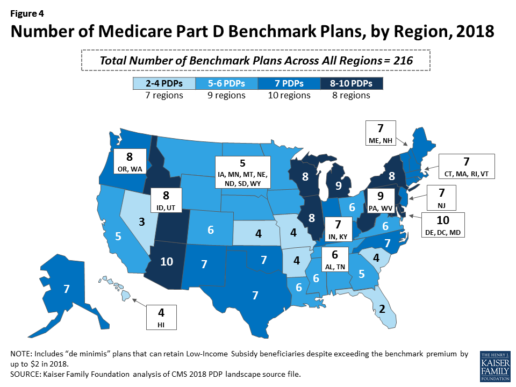

Benchmark plan availability varies at the Part D region level, with most regions seeing a reduction of 1 benchmark plan for 2018 (Figure 4). The number of premium-free plans in 2018 ranges from a low of 2 plans in Florida to 10 plans in Arizona and Delaware/Maryland/Washington D.C.

Part D Plan Premiums and Benefits in 2018

Premiums. According to CMS, the 2018 Part D base beneficiary premium is $35.02, a modest decline of 2% from 2017.2 Actual (unweighted) PDP monthly premiums for 2018 vary across plans and regions, ranging from a low of $12.60 for a PDP available in 12 out of 34 regions to a high of $197 for a PDP in Texas.

Part D enrollees with higher incomes ($85,000/individual; $170,000/couple) pay an income-related monthly premium surcharge, ranging from $13.00 to $74.80 in 2018 (depending on their income level), in addition to the monthly premium for their specific plan.3 According to CMS projections, an estimated 3.3 million Part D enrollees (7%) will pay income-related Part D premiums in 2018.

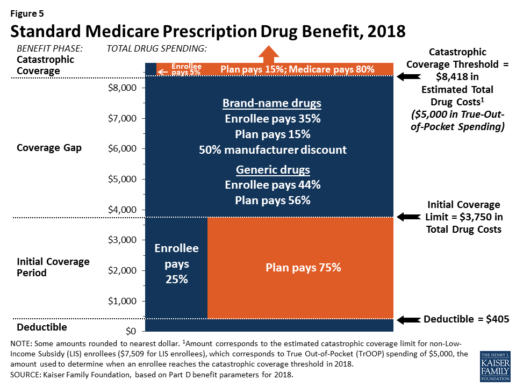

Benefits. In 2018, the Part D standard benefit has a $405 deductible and 25% coinsurance up to an initial coverage limit of $3,750 in total drug costs, followed by a coverage gap. During the gap, enrollees are responsible for a larger share of their total drug costs than in the initial coverage period, until their total out-of-pocket spending in 2018 reaches $5,000 (Figure 5).

After enrollees reach the catastrophic coverage threshold, Medicare pays for most (80%) of their drug costs, plans pay 15%, and enrollees pay either 5% of total drug costs or $3.35/$8.35 for each generic and brand-name drug, respectively.

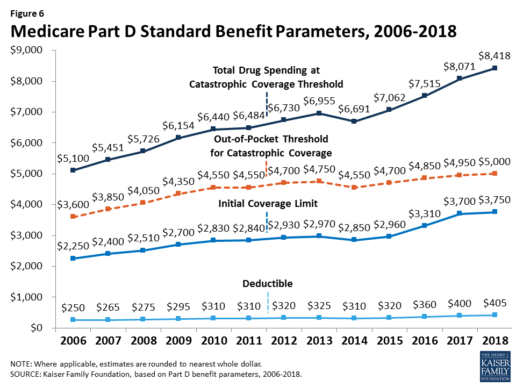

The standard benefit amounts are indexed to change annually by rate of Part D per capita spending growth, and, with the exception of 2014, have increased each year since 2006 (Figure 6).

Part D plans must offer either the defined standard benefit or an alternative equal in value (“actuarially equivalent”), and can also provide enhanced benefits. But plans can (and do) vary in terms of their specific benefit design, cost-sharing amounts, utilization management tools (i.e., prior authorization, quantity limits, and step therapy), and formularies (i.e., covered drugs). Plan formularies must include drug classes covering all disease states, and a minimum of two chemically distinct drugs in each class. Part D plans are required to cover all drugs in six so-called “protected” classes: immunosuppressants, antidepressants, antipsychotics, anticonvulsants, antiretrovirals, and antineoplastics.

In 2018, almost half (46%) of plans will offer basic Part D benefits (although no plans will offer the defined standard benefit), while 54% will offer enhanced benefits, similar to 2017. Most PDPs (63%) will charge a deductible, with 52% of all PDPs charging the full amount ($405). Most plans have shifted to charging tiered copayments or varying coinsurance amounts for covered drugs rather than a uniform 25% coinsurance rate, and a substantial majority of PDPs use specialty tiers for high-cost medications. Two-thirds of PDPs (65%) will not offer additional gap coverage in 2018 beyond what is required under the standard benefit. Additional gap coverage, when offered, has been typically limited to generic drugs only (not brands).

The 2010 Affordable Care Act gradually lowers out-of-pocket costs in the coverage gap by providing enrollees with a 50% manufacturer discount on the total cost of their brand-name drugs filled in the gap and additional plan payments for brands and generics. In 2018, Part D enrollees in plans with no additional gap coverage will pay 35% of the total cost of brands and 44% of the total cost of generics in the gap until they reach the catastrophic coverage threshold. Medicare will phase in additional subsidies for brands and generic drugs, ultimately reducing the beneficiary coinsurance rate in the gap to 25% by 2020.

Part D and Low-Income Subsidy Enrollment

Enrollment in Medicare drug plans is voluntary, with the exception of beneficiaries who are dually eligible for both Medicare and Medicaid and certain other low-income beneficiaries who are automatically enrolled in a PDP if they do not choose a plan on their own. Unless beneficiaries have drug coverage from another source that is at least as good as standard Part D coverage (“creditable coverage”), they face a penalty equal to 1% of the national average premium for each month they delay enrollment.

In 2017, more than 42 million Medicare beneficiaries are enrolled in Medicare Part D plans, including employer-only group plans.4 Of this total, 6 in 10 (60%) are enrolled in stand-alone PDPs and 4 in 10 (40%) are enrolled in Medicare Advantage drug plans. Medicare’s actuaries estimate that around 2 million other beneficiaries in 2017 have drug coverage through employer-sponsored retiree plans where the employer receives subsidies equal to 28% of drug expenses between $405 and $8,350 per retiree in 2018 (up from $400 and $8,250 in 2017).5 Several million beneficiaries are estimated to have other sources of drug coverage, including employer plans for active workers, FEHBP, TRICARE, and Veterans Affairs (VA). Yet an estimated 12% of Medicare beneficiaries lack creditable drug coverage.

Twelve million Part D enrollees are currently receiving the Low-Income Subsidy. Beneficiaries who are dually eligible, QMBs, SLMBs, QIs, and SSI-onlys automatically qualify for the additional assistance, and Medicare automatically enrolls them into PDPs with premiums at or below the regional average (the Low-Income Subsidy benchmark) if they do not choose a plan on their own. Other beneficiaries are subject to both an income and asset test and need to apply for the Low-Income Subsidy through either the Social Security Administration or Medicaid.

Part D Spending and Financing in 2018

The Congressional Budget Office (CBO) estimates that spending on Part D benefits will total $92 billion in 2018, representing 15.5% of net Medicare outlays in 2018 (net of offsetting receipts from premiums and state transfers). Part D spending depends on several factors, including the number of Part D enrollees, their health status and drug use, the number of enrollees receiving the Low-Income Subsidy, and plans’ ability to negotiate discounts (rebates) with drug companies and preferred pricing arrangements with pharmacies, and manage use (e.g., promoting use of generic drugs, prior authorization, step therapy, quantity limits, and mail order). Federal law prohibits the Secretary of Health and Human Services from interfering in drug price negotiations between Part D plan sponsors and drug manufacturers.6

Financing for Part D comes from general revenues (78%), beneficiary premiums (13%), and state contributions (9%). The monthly premium paid by enrollees is set to cover 25.5% of the cost of standard drug coverage. Medicare subsidizes the remaining 74.5%, based on bids submitted by plans for their expected benefit payments. Part D enrollees with higher incomes ($85,000/individual; $170,000/couple) pay a greater share of standard Part D costs, ranging from 35% to 80%, depending on income.

According to Medicare’s actuaries, in 2018, Part D plans are projected to receive average annual direct subsidy payments of $353 per enrollee overall and $2,353 for enrollees receiving the LIS; employers are expected to receive, on average, $623 for retirees in employer-subsidy plans.7 Part D plans’ potential total losses or gains are limited by risk-sharing arrangements with the federal government (“risk corridors”). Plans also receive additional risk-adjusted payments based on the health status of their enrollees and reinsurance payments for very high-cost enrollees.

Under reinsurance, Medicare subsidizes 80% of drug spending incurred by Part D enrollees above the catastrophic coverage threshold. In 2018, average reinsurance payments per enrollee are estimated to be $941; this represents a 7% increase from 2017. Medicare’s reinsurance payments to plans have represented a growing share of total Part D spending, increasing from 16% in 2007 to an estimated 41% in 2018.8 This is due in part to a growing number of Part D enrollees with spending above the catastrophic threshold, resulting from several factors, including the introduction of high-cost specialty drugs, increases in the cost of prescriptions, and a change made by the ACA to count the 50% manufacturer discount in enrollees’ out-of-pocket spending that qualifies them for catastrophic coverage. Analysis from MedPAC also suggests that in recent years, plans have underestimated their enrollees’ expected costs above the catastrophic coverage threshold, resulting in higher reinsurance payments from Medicare to plans over time.

Issues for the Future

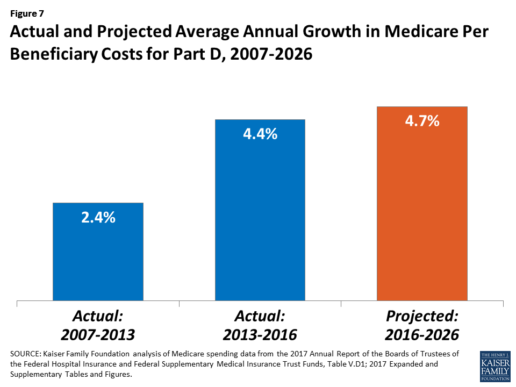

After several years of relatively low growth in prescription drug spending, spending has risen more steeply since 2013. The average annual rate of growth in Part D costs per beneficiary was 2.4% between 2007 and 2013, but it increased to 4.4% between 2013 and 2016, and is projected to increase by 4.7% between 2016 and 2026

(Figure 7).9

Medicare’s actuaries have projected that the Part D per capita growth rate will be comparatively higher in the coming years than in the program’s initial years due to higher costs associated with expensive specialty drugs, which is expected to be reflected in higher reinsurance payments to plans. Between 2017 and 2027, spending on Part D benefits is projected to increase from 15.9% to 17.5% of total Medicare spending (net of offsetting receipts).10 Understanding whether and to what extent private plans are able to negotiate price discounts and rebates will be an important part of ongoing efforts to assess how well plans are able to contain rising drug costs. However, drug-specific rebate information is not disclosed by CMS.

The Medicare drug benefit helps to reduce out-of-pocket drug spending for enrollees, which is especially important to those with modest incomes or very high drug costs. Closing the coverage gap by 2020 will bring additional relief to millions of enrollees with high costs. But with drug spending on the rise and more plans charging coinsurance rather than flat copayments for covered brand-name drugs, enrollees could face higher out-of-pocket costs for their Part D coverage. These trends highlight the importance of comparing plans during the annual enrollment period. Research shows, however, that relatively few people on Medicare have used the annual opportunity to switch Part D plans voluntarily—even though those who do switch often lower their out-of-pocket costs as a result of changing plans.

Understanding how well Part D is working and how well it is meeting the needs of people on Medicare will be informed by ongoing monitoring of the Part D plan marketplace and plan enrollment; assessing coverage and costs for high-cost biologics and other specialty drugs; exploring the relationship between Part D spending and spending on other Medicare-covered services; and evaluating the impact of the drug benefit on Medicare beneficiaries’ out-of-pocket spending and health outcomes.

Endnotes

- Poverty and resource levels for 2018 are not yet available (as of September 2017).

- The base beneficiary premium is equal to the product of the beneficiary premium percentage and the national average monthly bid amount (which is an enrollment-weighted average of bids submitted by both PDPs and MA-PD plans). Centers for Medicare & Medicaid Services, “Annual Release of Part D National Average Bid Amount and Other Part C & D Bid Information,” July 31, 2017, available at https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/PartDandMABenchmarks2018.pdf.

- Higher-income Part D enrollees also pay higher monthly Part B premiums.

- Centers for Medicare & Medicaid Services, Medicare Advantage, Cost, PACE, Demo, and Prescription Drug Plan Contract Report – Monthly Summary Report (Data as of August 2017).

- Board of Trustees, 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds, Table IV.B7, available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2017.pdf.

- Social Security Act, Section 1860D-11(i).

- 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds; Table IV.B9.

- Kaiser Family Foundation analysis of aggregate Part D reimbursement amounts from Table IV.B10, 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.

- Kaiser Family Foundation analysis of Part D average per beneficiary costs from Table V.D1, 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.

- Kaiser Family Foundation analysis of Part D benefits spending as a share of net Medicare outlays (total mandatory and discretionary outlays minus offsetting receipts) from CBO, Medicare-Congressional Budget Office’s June 2017 Baseline.

Read the full article here.

Source:

Kaiser Family Foundation (2 October 2017). “The Medicare Part D Prescription Drug Benefit” [Web Blog Post]. Retrieved from address https://www.kff.org/medicare/fact-sheet/the-medicare-prescription-drug-benefit-fact-sheet/#26740